Bauer has been warning readers for years about the downfalls of opting-in to “courtesy” overdraft protection. And with good reason. In 2021, estimated overdraft fees charged by U.S. banks for this “courtesy” exceeded $8 billion.

You’ve probably been noticing lately that a lot of banks are lessening the sting of these fees, or eliminating them entirely. That’s the result of a concerted effort by the Biden administration and regulators. Most notably, Michael Hsu, the Acting Comptroller of the Currency (OCC), is actively seeking an end to fees that take advantage of the “financially vulnerable”.

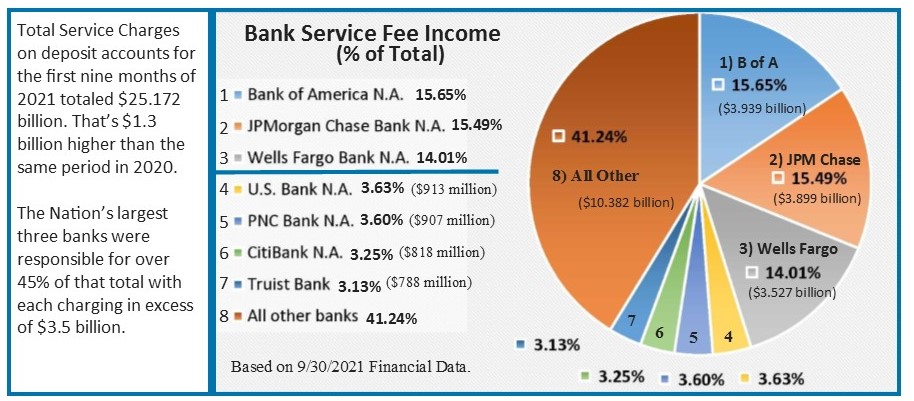

Most banks aren’t required to itemize their consumer service fees, but, for the most part, Big Banks are required to do so. And from that data, we can tell you that the nation’s largest three banks (by asset size) charge over 45% of all consumer fees on deposit accounts (see page 2 chart), although, the way they collect these fees does vary.

4-Star Wells Fargo Bank N.A., has by far, the most income from overdraft fees; 5-Star Bank of America reportedly cut its overdraft fees from $35 to $10, but when it comes to both maintenance fees and ATM fees, BofA takes the lead. After giving consumers a grace day before charging an overdraft fee, 5-Star JPMorgan Chase Bank N.A., the nation’s largest bank, is now the king of “All Other Service Charges on Deposit Accounts”.

4-Star CitiBank N.A., the nation’s fourth largest bank, is much more consumer friendly when it comes to fees. While its asset size is not much smaller than that of JPMorgan Chase, its services charges as a percent of total transaction and savings deposits is just 0.08% (annualized), compared to 0.21% at JPMorgan Chase. (The median is 0.12%.) Page 7 has a list of the 50 with the highest percent.

5-Star Truist Bank, the 6th largest U.S. Bank, recently announced plans to restructure many of its accounts and fees. It will provide a $100 buffer for small overdrafts and a line of credit of up to $750 for larger infractions. Truist will make up lost fee revenue by closing as many as 800 branch offices. But that was already slated to happen when BB&T and SunTrust merged in December of 2019.

Then there are other banks that are touting no overdraft fees or charges of any kind on deposit accounts, but they are making money through other fee income. 4-Star Capital One is a perfect example because Capital One makes its money through credit cards. Another, 5-Star Ally Bank, specializes in dealer financial services (financing, leasing, commercial insurance, and such).

So, while we want to applaud the banks that are taking the initiative to lower fees on checking accounts, we do have to keep an eye out for where other fees may pop up.

In other news, the OCC just issued conditional approval for the large fintech company, SoFi Technologies to become a national bank. The Fintech will acquire 5-Star Golden Pacific Bank, N.A., Sacramento, CA. SoFi Bank intends to inject $750 million in capital to pursue its national digital plan, while maintaining Golden Pacific’s three branches and community bank business.

Fintech competition is another great reason for bankers to be looking at reducing their fee income. We expect that competition to get even more intense as time goes on.

2 comments on “3 Banks Charge 45% of All Consumer Service Fees”

Comments are closed.