All Credit Union and Bank Star-Ratings are now updated based on June 30, 2024 Financial Data. Next week we will touch more on the state of the credit union industry.

This week's focus is on overall bank loan quality. The banking industry increased loan loss provisions by $23.3 billion in the second quarter 2024, yet the coverage gap is widening as delinquent loans climb.

As a result, there are 51 banks listed on page 5 of this week's Jumbo Rate News that show signs of stress, although in different areas and to differing degrees.

A Loan is a Great Asset (for a Bank), Unless it’s Not

As promised, this week we begin to dive into the loan quality pressures that banks are now confronting. But before we get into that dreary topic, let’s start with something lighter:

All Credit Union Star Ratings are updated on bauerfinancial.com, based on June 30, 2024 financial data.

As has been the trend for some time, the biggest credit unions are getting bigger while smaller credit unions struggle to maintain their membership. In fact, the 442 biggest credit unions, those with assets exceeding $1 billion, now control 77% of all industry assets. We’ll discuss credit unions more next week. For now, back to banks.

Last week we touched on some of the problem areas that banks are facing in their loan portfolios. We’ll get into the details of which loan types are souring and where, but today we are looking at overall nonperforming loans. The 51 banks listed on page 5 all show signs of stress, but to differing degrees.

To create that list, in addition to being rated less than 4-Stars by Bauer, each bank has:

a) either a Bauer’s adjusted capital ratio (CR) of less than 2% (there are 15 of those) OR b) nonperforming assets exceeding 2.5% of tangible assets (bringing the pool up to 87), AND sufficient loan loss allowances to cover less than 60% of their delinquent loans (which brings it back down to 51).

Provisions for credit losses totaled $23.3 billion in the second quarter. That is $2.7 billion more than the first quarter and marks the eighth consecutive quarter that provisions have exceeded pre-pandemic levels. In spite of increased provisioning, however, we lowered our threshold for this list (from 80% of delinquent loans in January (JRN 41:04), the last time we published a similar list of banks) to just 60% today.

With an industry increase of 22% in nonperforming loans during the 12 months ending June 30, 2024, the coverage gap is widening, in spite of that sizeable increase in reserves. The banks on page 5 all have well below the industry weighted average coverage ratio of 194%.

You may notice there is only one Zero-Star bank listed on page 5, and it is one we reported on in January. Back in 2022, First & Peoples B&TC, Russell, KY made an ill-conceived shift in its lending strategy. What was primarily pristine consumer loans became “not-so-pristine” loans to “nondepository financial institutions” (i.e. fintechs).

We should mention that First & Peoples’ June 30th Call Report data looks somewhat better than that of March 31st. Whether this is the beginning of a turnaround is not clear yet. The bank has posted losses in four of the last five quarters; its Bauer’s Adjusted Capital ratio is –1.56%; and its Texas Ratio is 127.26%. It is not a pretty picture from what we see.

Another repeat from the January list, 3-Star Eastern Savings Bank, FSB, Hunt Valley, MD, has an entirely different story to tell. Its loan portfolio contains high amounts (43%) of Commercial Real Estate (CRE) and 1-4 family residential mortgages (39%). That translates to 82% of repossess“able” property. But, no banker wants to repossess property.

It is much better for all concerned to work these loans out. That said, even a worst case scenario (i.e. a complete write-off of the $15.746 million) would result in a leverage capital ratio remaining well north of 20%.

Historically, Eastern SB’s short term past due loans seem to fluctuate with the seasons. One quarter past due loans may total $8 million; the next quarter they can be down to $2 million. The longer term (90 days+) delinquencies are much more consistent.

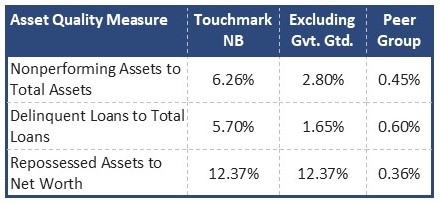

Now let’s take a look at a bank that’s new to the list, 2-Star Touchmark National Bank, Alpharetta, GA, a $481 million asset bank that was established in January of 2008 (just before the housing bubble burst). In spite of that inauspicious start-date, Touchmark NB has made it through. Well over 300 banks that were active at that time would not survive to see 2011, but Touchmark NB did.

Touchmark NB does not have a diversified loan portfolio (perhaps because of that housing bubble). Its loans are almost entirely (91%) CRE. You could call this another piece of poor timing, but Touchmark NB has been an active Small Business Administration (SBA) lender for years. A benefit that comes with that is that many of its loans are government guaranteed. Let’s take a look at the numbers:

While still considerably higher than the peer group, government guarantees make a big difference in Touchmarks’ delinquency ratios. However, none of the repossessed assets carry those guarantees. There’s more:

In April 2024, the OCC issued a particularly scathing enforcement action against Touchmark NB. The 31 page document addressed a number of shortcomings including (among other things): liquidity management; interest rate risk management, problem loan management and “management-management”. It has some work to do.