The Federal Reserve held rates steady at its Open Market Committee Meeting last week, but we don’t believe that will be the case next month. We expect a nice little Holiday gift of another 25 basis point increase when they convene for the final time this year on 12/19.

When interest rates change, up or down, but in this case up, bankers are faced with a balancing act. Longer term assets (like mortgage loans) will continue to earn based on the lower rates, while new loans (and deposits) will be booked at higher rates. In this environment, there are two crucial things to consider:

1) Rates are still going up, so at some point in the not too distant future, today’s loans will be earning less, comparatively speaking.

2) In order to fund new loans, banks will have to pay higher interest on deposits.

In this issue, we take a look at how our nation’s banks handle this precarious balancing act. When changes in interest rates are slight, an increase in loan volume might suffice, but when they are regularly changing, it becomes more challenging. To make up for volatility in net interest margins, effective management of noninterest income is even more significant.

According to the FDIC’s Quarterly Banking Profile for the second quarter, noninterest income at all U.S. banks was up 2% (or $1.3 billion) over a year earlier. That increase, it further stated, was mainly attributable to servicing fees that rose 29½% ($638.2 million) over the 12 month period.

In fact, over 55% of all U.S. banks reported higher noninterest income in the second quarter 2018 compared to a year ago. However, noninterest expense rose 4.6% or $4 billion during the same period. So, not only have bankers been challenged in recent years with small net interest margins, noninterest expenses are now climbing as well.

When we think of noninterest income, the first that comes to mind is usually service charge income, but there are several other components: fiduciary duties, trading revenue, servicing fees, to name a few.

According to June 30th call reports, the banks listed on page 7 had the highest noninterest income among community banks. 4-Star Nationwide Bank, OH (#3), for example, did not report any income from overdraft fees, maintenance fees or any service charges on deposit accounts. Its non-interest income came entirely from fiduciary activities.

5-Star First Financial Bank, N.A., TX (#19), on the other hand, earned $10.259 in noninterest income, 30% of which came from service charges on deposit accounts. The rest derived mainly from a mixture of loan and lease sales, commissions and fees on brokerage and insurance activities, and sales of repossessed real estate (REO).

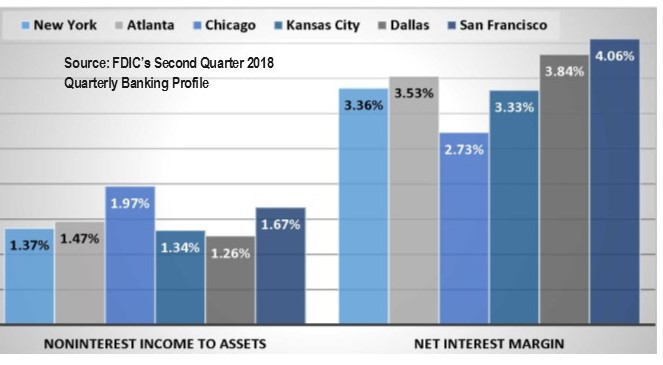

We combined the two items (noninterest income and net interest margin) on the chart below to give an idea of why some banks may charge higher fees than others. You can see the Chicago (or Midwest) Region charges the highest percent of noninterest income to assets. It also has the lowest net interest margin of all the regions. The opposite is true for the Dallas (Southwest) Region. These banks derive the least from noninterest income but their net interest margins, as a whole, are the second highest in the nation.

San Francisco is the stand-out. Banks in the Western Region charge more than the national average on both fronts: noninterest and interest income. The Western Region also contains Utah, the state with the majority of Industrial Loan Banks (ILCs). ILCs are NOT community banks, so you won’t find any listed on page 7. As a rule, ILCs tend to have high noninterest income, not necessarily from service charges, or any of the other items we mentioned, but from “other” sources.