Credit union financial data is typically released by regulators about two weeks after bank data, but this time it took more than three weeks. While we have no control over when the regulators make the data available, we dedicate ourselves to getting the institutions through the evaluation process as efficiently as possible. As a result, all credit union star-ratings were updated on bauerfinancial.com on Saturday, 6/9.

Shares and deposits increased by $65.5 billion (5.8%) from March 31, 2017, ending the first quarter 2018 at $1.204 trillion. While that number pales in comparison to the nation’s banks (roughly 10%), it has been growing steadily for years. In fact, the largest three U.S. banks each have deposits totaling more than the entire credit union industry. They are:

- JPMorgan Chase, OH at $1.559 trillion;

- Bank of America, NC at $1.410 trillion; and

- Wells Fargo Bank, SD at $1.358 trillion.

Membership has been increasing at an even higher rate than shares indicating that new members are joining with smaller dollar balances. During the 12 month period ending March 31st, we lost 207 federally insured credit unions (3.6%). Most of the reduction was due to mergers and is, according to the National Credit Union Administration (NCUA), consistent with long-running consolidation trends.

We can attest to that as well. Although two credit unions did fail in the first quarter: Zero-Star First Jersey Credit Union, Wayne, NJ was closed on February 28th while N.R. St. Elizabeth’s Credit Union in Chicago failed on January 30th. A third, Zero-Star Ukrainian Future Credit Union, Warren, MI, was placed into NCUA conservatorship.

None of that withstanding, over 80% of the industry is recommended by Bauer (i.e. rated 5-Stars or 4-Stars). (On page 7 you will find a state-by-state list of Recommended vs. Troubled and Problematic (T&P) credit unions (those rated 2-Stars or below). At 2.6% of the total, the percent of CUs rated 2-Stars or below has risen a bit from a year ago (2.4%). At March 31, 2017, 139 credit unions fell into this category while today we have 148.

We are pleased to report that sixteen states plus Puerto Rico have no T&P Cus at all. There are nearly 500 reporting credit unions that are not rated (N.R.) by Bauer because they are either too small (less than $1.5 million in assets) or do not carry federal deposit insurance. There are also nine de novo credit unions that are too new to rate (S.U.). Of the nine: three are community credit unions; three have a faith-based common bond; two have a government common bond and the final one has multiple common bonds.

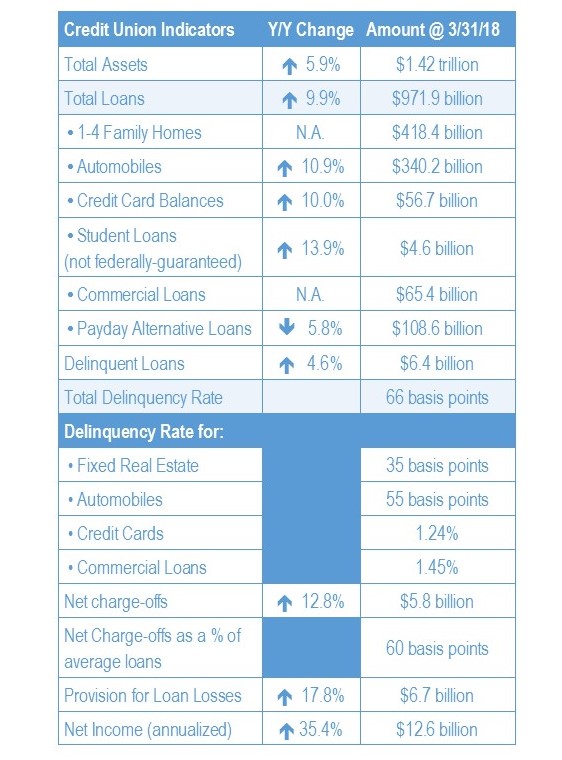

Total assets are up 5.9% from a year ago ending the first quarter at $1.42 trillion. Of that, $971.9 billion is in loans as most major loan categories posted gains over the year earlier. The exception was Payday Alternative Loans (PALs) which were down 5.8% from last March. A possible explanation for the decline in PALs is the increase in the Fed Funds Rate (which was bumped up another quarter point on Wednesday). The interest rate on PALs vary by institution but most fall between 18 & 28%.

The net interest margin (NIM) at the nation’s credit unions is not suffering from these rate hikes, though. In fact, the opposite is true. The NIM increased in each of the last four quarters and ended the first quarter 2018 at 3.03% as a percent of average assets. See the chart to the right for additional highlights from credit union first quarter filings.