The FDIC likes to put a positive twist on its quarterly data press release, but we know well enough to look beyond.

Aside from tightening interest margins and deterioration in credit card and CRE loan quality, the industry has witnessed a large-scale migration from non-interest bearing deposits to interest bearing deposits.

This week, we specifically focus on banks where the growth in interest-bearing deposits far exceeded the overall deposit growth. You will find 50 such banks listed on page 5 of this week's Jumbo Rate News.

All New Bank Star-Ratings this Week

All bank star-ratings in Jumbo Rate News as well as on our website, bauerfinancial.com, are now based on first quarter 2024 financial data. (Credit union ratings and data will be forthcoming.)

We’ve been around long enough to know that the FDIC likes to put a positive twist on its media release. We also know, the numbers don’t lie. The FDIC’s Quarterly Banking Profile (QBP) included the following numbers and a couple of surprising words from the FDIC (in quotes):

A tightening net interest margin:

The first quarter industry net interest margin (NIM) of 3.17% is 10 basis points lower than the previous quarter and 7 basis points below the pre-pandemic average.

Depending on the type of institution, this average can be very misleading. For example, credit card banks average NIM is 10.59% while the average NIM at mortgage lenders is a paltry 1.57%.

“Material deterioration” in credit card and CRE loans (that’s the one):

At 1.59%, the noncurrent loan rate for non-owner occupied commercial real estate (CRE) is at its highest level since the fourth quarter of 2013. Office loans at the nation’s biggest banks are the primary cause.

The credit card charge-off rate of 4.7% at March 31st, 2024, is 55 basis points higher than at year-end ’23 and is at its highest point since the third quarter of 2011.

An increase in problem banks:

The total number of FDIC-insured banks declined by 19 during the first quarter, however, the number of problem banks increased by 11 (from 52 to 63). Assets at those problem banks increased 420% - from $15.8 billion to $82.1 billion.

An increase in noncurrent loans:

Short term delinquent loans (those 30-89 days past due) grew 11.5% from first quarter 2023, while noncurrent loans (90 days or more delinquent) increased by 23%. Restructured loans, which total $40,355 million, represent a 214.3% increase over 1st quarter 2023.

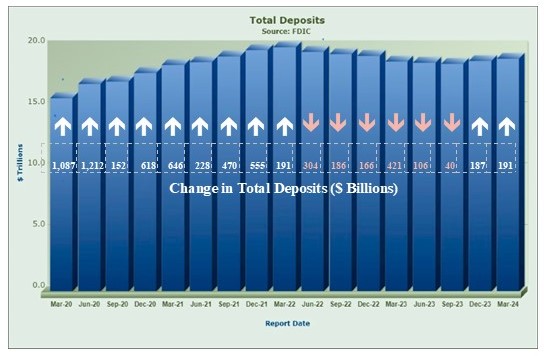

We will be diving more deeply into all of this in coming weeks. This week our primary focus is deposits, which had been on a downward spiral for a year and a half.

At March 31, 2024, bank deposits posted a second quarterly increase. Those two gains were enough to bring the year-over-year deposit change to a positive 1.4%. (This made it easier to fund the 1.7% year-over-year increase in total loans.)

In addition to gaining deposits, there has been a large-scale migration from non-interest bearing deposits to interest bearing deposits. This was not included in the QBP, but according to the call report data, industrywide interest bearing deposits increased over 6% over the year, while non-interest bearing deposits decreased more than 12%.

To demonstrate, the 50 community banks on page 5 each grew total deposits during the 12 month period ending March 31, 2024. However, in each case, interest-bearing deposits increased while noninterest bearing deposits decreased. The growth in the interest-bearing deposits far exceeded the overall deposit growth. (Each of the banks listed was also established prior to 2019 and has total assets in excess of $150 million.)

There are actually well over 1,400 community banks that match this criteria, but these are the 50 with the greatest percent of interest bearing deposit growth. They range from 269% (highest) to 42.7% (#50). Let’s start with the highest.

5-Star Classic Bank, N.A., Cameron, TX reported the highest growth in interest bearing deposits at 269.3%. Classic Bank began taking in brokered deposits in the first quarter 2023 when it reported slightly more than $5 million in brokered deposits (less than 1% of total deposits). By this March 31st, one year later, its brokered deposits had grown to $27.5 million representing 4.5% of total deposits. In itself, that’s not worrisome, but as a rule, brokered deposits require higher interest rates than other deposits.

It can be a high price to pay to maintain the bank’s deposit base.

Unlike Classic Bank, 5-Star Virginia NB, Charlottesville, VA has no brokered deposits. Its assets and deposits grew at a slow pace over the 12-month period ending March 31st. (2.99% and 2.32%, respectively). However, its interest bearing deposits ballooned over 78%. Much of that appears to have been caused by transfers from non-interest bearing accounts, which had a drop of nearly 53%. Virginia NB’s loans, however, grew over 20% during those same 12 months.

Next week we will look at the effect this deposit migration has had on net NIM.