At $42.2 billion, loan loss provisions for the first half of 2023 were nearly 160% higher than the first half of last year. As an industry, banks are well-provisioned to handle any upcoming downturn. However, not all individual banks can say the same.

Bauer's Historical Bank Generator Report Provides side-by-side financial data for 5 quarters of your choice (compare year-ends or historical year-over-year quarters) on any FDIC-Insured U.S. bank. This report includes balance sheet and income statement data (including provisions for loan losses) as well as a number of key ratios and peer comparisons.

All New Bank Star-Ratings this Week

All bank star ratings are now based on June 30, 2023 financial data. (New credit union ratings will be out shortly.) Here are some of the highlights from the new bank data:

Two New De Novo Banks

3½-Star Beach Cities Commercial Bank, Irvine, CA opened its doors for business on June 12, 2023. Its approval for deposit insurance required a minimum of $25 million in paid-in capital and a minimum leverage capital ratio (CR) of 8%.

At June 30th, Beach Cities Commercial Bk reported total assets of $34.938 million and a leverage capital ratio (CR) of 385.77%.

3½-Star Community Unity Bank, Birmingham, MI opened for business just before quarter end, June 26th to be exact. Its approval required capital of $23.204 million, slightly less than that of Beach Cities, with the same 8% leverage CR. Total assets at the close of the quarter were $27.172 million and its leverage CR was 1853.6%.

One Bank Failed in Q2

First Republic Bank, San Francisco, CA failed on May 1st and was closed by the California Department of Financial Protection and Innovation, which turned it over to the FDIC as receiver. First Republic marked the third regional bank failure this year and the second in California. The previous two failures of course being Silicon Valley Bank (also known as SVB), CA and Signature Bank, NY, both of which failed in March.

With roughly $229 billion in assets and $103.9 billion in total deposits, there was a limited pool of possible buyers. Stepping up to the plate was 5-Star JPMorgan Chase Bank N.A., Columbus, OH, the nation’s largest bank. Now, with more than $3.7 trillion in consolidated assets, JPMorgan Chase & Company is more than half a billion $ larger than its closest competitor.

49 Banks Rated 2-Stars or less

For the first time we can remember no banks received a regulatory capital classification of less than “Adequate” based on June 30, 2023 financial data. And, only eight are classified as “Adequate”; the rest are considered “Well-Capitalized” by regulatory standards. (Not by Bauer.)

However, Well-Capitalized or not, the 49 banks listed on page 5 of this week’s Jumbo Rate News are each rated 2-Stars (or lower) based on June 30, 2023 financial data. These banks represent just 1.06% of all U.S. banks and just 0.05% of industry assets.

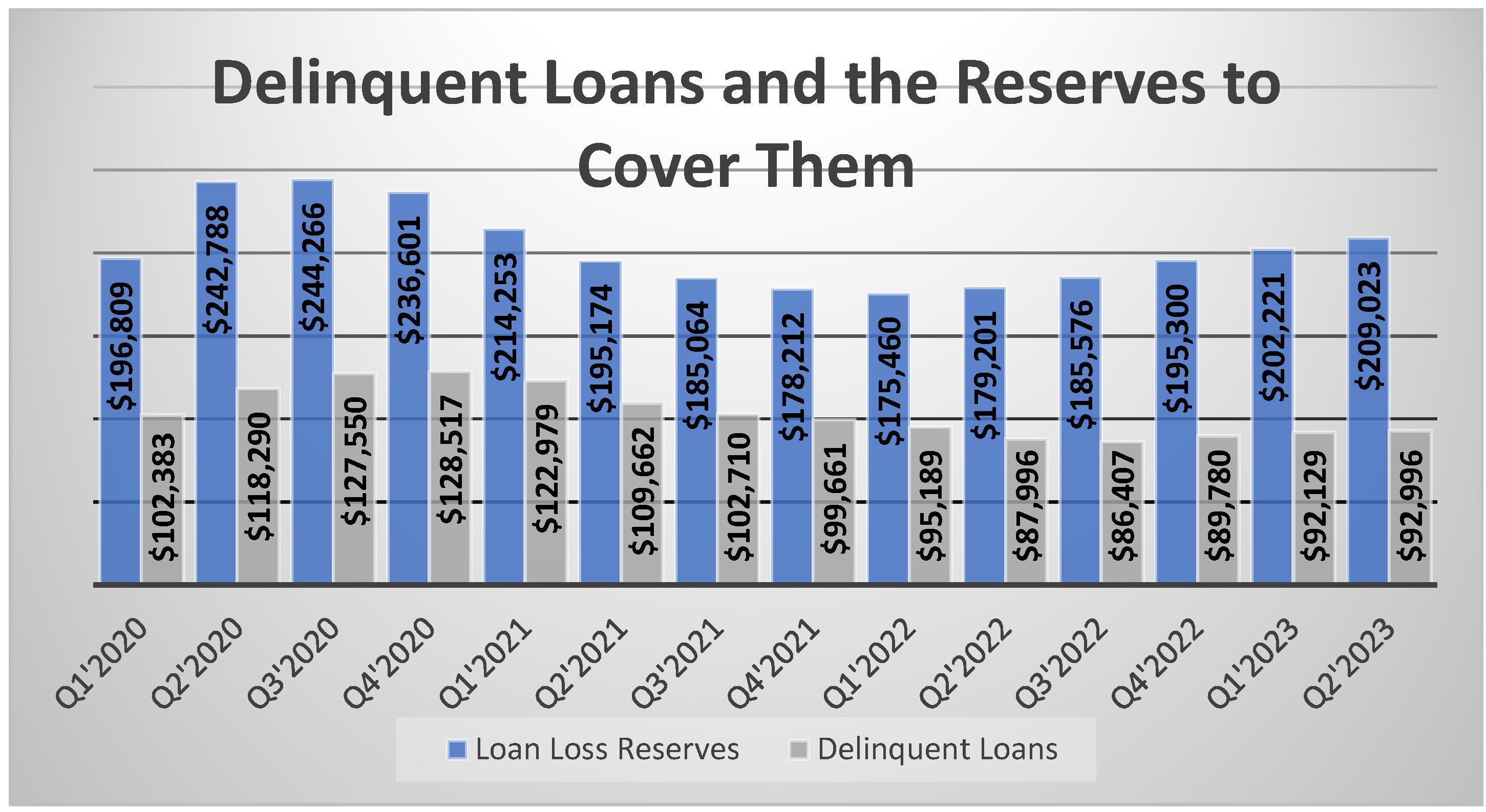

Banks Increasing Loan Loss Reserves

Our nation’s banks set aside more than $21 billion in the second quarter to boost loan loss provisions. Provisions for the first half of 2023 totaled $42.2 billion. That’s nearly 160% higher than the first half of last year, which was $16.3. It still comes in far short of the first half of its 2020 peak of $114.6 billion, but as delinquencies continue to rise, so too shall loan loss reserves.

Both are well below the levels seen during the height of the pandemic. However, both are also on the rise again. As the chart illustrates, banks as an industry are well-provisioned to handle a downturn. However, not all individual banks can say the same.