A study released last month by the FDIC regarding the “Structure, Performance, and Social Impact” of Minority Depository Institutions (MDIs) included some interesting information, but left some out as well. An MDI can be either a) at least 51% owned by minorities, or b) the majority of the board and community it serves is predominantly minority.

As the communities that housed MDIs were historically underserved by other banks, it was important to preserve the numbers of MDIs as well as the minority characteristics in the event of a merger. That being said, of the nine MDIs that have disappeared since the end of 2017, only three were merged into other MDIs (see page 7). The one MDI that had multiple minority ownership a year ago (State Bank of Georgia) voluntarily closed last July. It did not find a merger partner or acquirer.

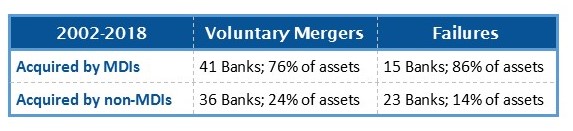

These are just the most recent actions. The FDIC reported a better success rate over the long-term.

According to the study, MDI financial performance improved significantly over the past five years. We concur with that finding, but the entire industry has improved significantly. Based on March 31,2019 financial data, there are 70 banks on Bauer’s Troubled and Problematic Bank Report; 11 (15.7%) are MDIs. They are listed on page 7.

Consistent with the rest of the industry, the study found that MDI branch offices are also declining, particularly Hispanic American and African American MDIs. The exception to the rule is Native American MDIs, which operate several more branches today than they did in 2013.

About half of all MDI charters and a little more than half of their assets are Asian American. Their share has been steady increasing this century; they held just 23% of total MDI assets in 2001. While African American and Native American MDIs control 15% and 13%, respectively, of the MDI charters, each hold just about 2% of total MDI assets.

Perhaps the most surprising piece of the FDIC study did not relate to the size of the institutions, but rather the composition of their loan portfolios. About 25% of non-MDI community banks are Commercial Real Estate (CRE) Specialists. For MDIs, that number jumps to 60%. This was particularly critical during the last recession, when institutions with high CRE concentrations fared much worse than their counterparts.

During the course of the study, the FDIC reports that MDIs were 2½ times as likely to fail as other banks. In fact, between year-end 2001 and year-end 2018, 40 MDIs failed. That’s 7.3% of total bank failures. And while many new MDIs were chartered in the early 2000s, none have opened since 2008. There is one, MOXY Bank, Washington, DC (JRN 36:22) that received FDIC approval in January and is expected to open this year. As of this writing, it is still working on raising the $25 million in capital it needs to do so.

Since MDI is a voluntary designation, existing institutions can apply for the designation if they qualify. They can also lose the status if their ownership changes. So, for example, in 2018, three banks newly gained MDI status while one lost it. This does make it difficult to track their performance as a group.

But, according to the study, MDIs tend to outperform non-MDI community banks in revenue generation, including net interest income and noninterest income. Higher yields on earning assets offset higher interest expense, particularly on the smaller MDIs, which tend to be African or Native American.