Fact: Bank Service Charges have decreased more than 9% in the past 5 years.

Top Offenders: While Bank of America and some other Big Banks have been popular targets for regulators, they are not the biggest offenders, at least not when measured as a percent of deposits. The 50 worst offenders as a percent of savings and transaction deposits can be found on page 5 of this week's Jumbo Rate News.

Other Resources: LLAMAS Report Bundle will let you know if a bank has been cited by its primary regulator with a formal enforcement action.

BofA Caught Double Dipping

On July 11th, both the Office of the Comptroller of the Currency (OCC) and the Consumer Financial Protection Bureau (CFPB) issued consent orders against 4-Star Bank of America, Charlotte, NC in regards to the bank’s overdraft practices.

According to the OCC, between March 2020 and November 2021, BofA charged tens of millions of dollars by resubmitting payments that had already been denied due to insufficient funds (NSF). Each time the payment was resubmitted, it would incur another $35 penalty (either as a NSF or an overdraft fee). These multiple fees for a single transaction are a clear violation of the Federal Trade Commission Act’s prohibition against unfair and deceptive practices.

Bank of America agreed to pay $60 million to the OCC to settle this matter. But that’s not the end of this story. On the same day, and in conjunction with the OCC order, the CFPB issued its own consent order against the globally systemically important Bank of America.

According to the CFPB, BofA not only double dipped, allowing multiple fees to be repeated for the same transaction, it also withheld credit card points and cash rewards and even opened unauthorized accounts without the consumers’ consent or knowledge.

These claims date back as far as 2012 and reportedly harmed hundreds of thousands of consumers. For that, BofA has agreed to pay $100 million directly back to those harmed as well as another $90 million in penalties to the CFPB. That’s a total of $250 million. You’d think that would get the point across but there are no guarantees.

This is not BofA’s first rodeo. Here are just a of the few civil money orders that have been issued against BofA due to activities that were particularly harmful to consumers:

- 2014—ordered to pay $727 million for illegal credit card practices (CFPB);

- 2022—illegal garnishments cost it another $10 million (CFPB);

- 2022—faulty disbursement of unemployment benefits during COVID cost it $225 million (CFPB) and $125 million (OCC).

Most banks don’t have to report their service charges. Of those that do, BofA, which is the second largest U.S. bank by deposits, does not charge anywhere near as much in overdraft fees as some of its peers.

In the first quarter 2023, BofA charged $33 million in overdraft fees alone; 5-Star JPMorgan Chase Bank, the largest U.S. bank charged $297 million; and 4-Star Wells Fargo Bank, SD, the third largest, charged $224 million. Even 4-Star Truist Bank, NC, which is less than a quarter of the size of BofA, charged $81 million in overdrafts.

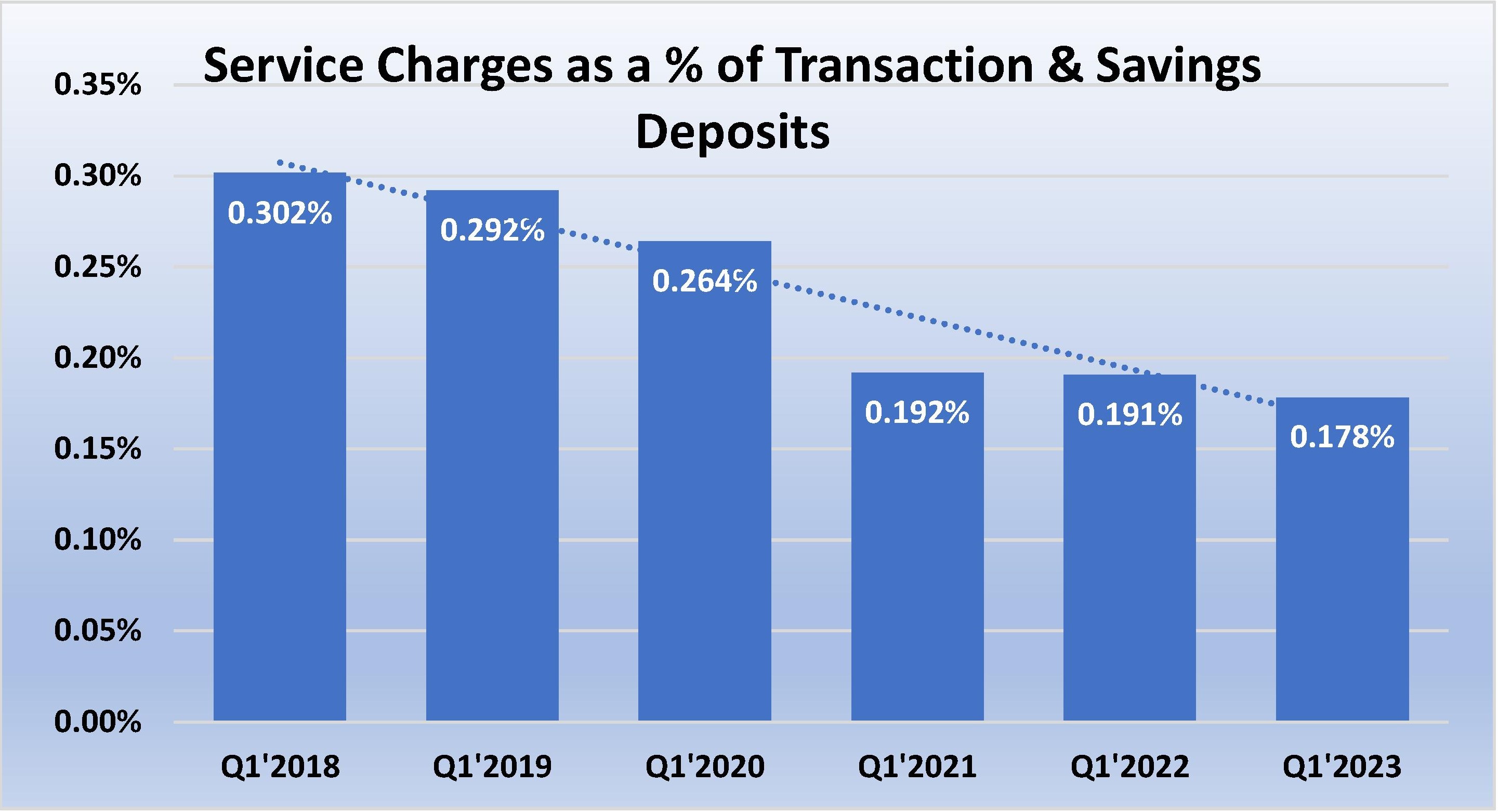

When we add all of the service fees together (overdraft, maintenance, ATM fees and other fees), BofA’s total at 3/31/23 (annualized) was just 0.178% of its transaction and savings deposits. The national average is also 0.178%. JPMorgan’s was a little higher at 0.200%, Wells Fargo was even higher at 0.307% and Truist was in between the two and 0.259%.

On page 5, however, we have listed the 50 banks that gained the most in service charge income (annualized) as a percent of their transaction and savings accounts based on first calendar quarter 2023 financial data. For reference, BofA would be #1,685 on the list.

Silvergate, the first bank on the list, doesn’t count as it is the process of self-liquidating.

3-star Vermont State Bank, IL, which follows Silvergate on page 5, is a tiny community bank with 1 office in the dwindling village of Vermont in southwestern Fulton County, Illinois. Established in 1947, Vermont State Bank lost about 13% of its assets in the 12 months ending March 31, 2023; it has been reporting losses for the last three years; and its loan quality is anything but stellar.

Its service charge income is less than $200,000 but its deposits have shrunk along with the village’s collective billfold.

Vermont State Bank is the exception, though, not the rule. In the past five years, total deposits at U.S. Banks have grown by 40%. Transaction and savings accounts have grown slightly more than the total as CDs lost favor for several years. They are making a comeback now with higher rates.

The service charge income on transaction and savings accounts has decreased over 9% in those same five years. Today’s 0.178% average service fee number is down from 0.302% at March 31, 2018. All of the banks listed on page 5 are well above both of those numbers.

It does appear the civil money penalties are paying off. Even though BofA is not the most egregious offender, it casts a long shadow. Good job regulators for reigning these in.

1 comment on “BofA Caught Double Dipping”

Comments are closed.