Last week (JRN 36:16) we brought you through 1989 and the passage of FIRREA demonstrating how the relationship between brokers and bankers turned sour. This week, we’ll take a quick look at the next 20 years, beginning with the passage of the FDICIA (Federal Deposit Insurance Corporation Improvement Act of 1991).

The FDICIA created the “Prompt Corrective Action” (PCA) which assigns the regulatory capital classification that we’re accustomed to seeing now. Before this, a bank could accept brokered deposits as long as it was not deemed “Troubled”. Now, instead of merely not being “Troubled”, a bank has to be “Well-Capitalized” (it can also be “Adequately Capitalized” with a special waiver) in order to accept brokered deposits.

Regulators were finally realizing the value of Bauer’s tough standards, although Bauer’s were (and still are) tougher. These new PCA rules took away incentives for unscrupulous brokers. Most left CD placement for more lucrative endeavors. Those that remained generally placed deposits in the best interest of their clients

Fast forward to 2003: reciprocal deposits are born. These are deposits that a bank receives via a network in return for placing the same amount of deposits at other network banks. This system enables customers to place virtually limitless amounts of insured deposits with just one transaction. The network does the work of splitting them between the banks and ensuring they are fully insured.

Because reciprocal deposits are complex and are often managed through a third-party sponsor, regulators viewed them as brokered deposits. Right or wrong, it was that way until the passage of the Economic Growth, Regulatory Reform and Consumer Protections Act (EGRRCPA) last May.

EGRRCPA allows a capped amount of reciprocal deposits to be exempted from treatment as brokered deposits …at certain institutions …and under certain circumstances (i.e. well-capitalized and well rated banks). Beginning with March 2019 data, a significant amount of reciprocal deposits will be excepted from the broker definition and restrictions.

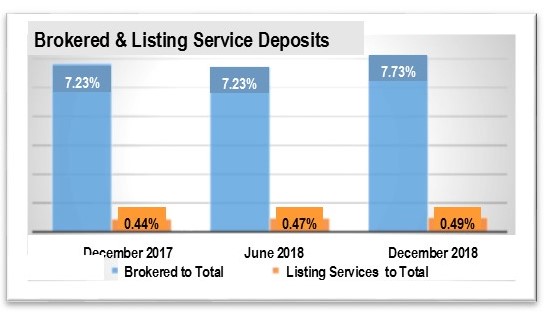

Since EGRRCPA was passed last year, brokered deposits have risen. It will be interesting to see how this changes with the March data and the new rules. The chart shows brokered deposits and listing service deposits as a percent of total deposits before the bill was signed, after it was signed, and again six months later.

At year-end 2018, 41% of banks held some amount of brokered deposits, the vast majority of brokered funds, however, (almost 90%) are held by just 100 Banks. What’s more important than volume, though, is how much dependence a bank has on brokered deposits, since they may not always be available.

Last week we looked at which banks had the most brokered deposits in terms of volume. This week we are looking at banks that have the highest % of brokered deposits relative to total deposits (page 7). As a reference, peer group averages range from 1.68% at the smallest banks to 11.18% at the largest institutions. Brokered deposits represent more than 90% of total deposits at six of the banks listed on page 7 and between 50% and 90% at another 23 banks. This could be a problem in a market downturn, or in a case like 3-Star Talbot State Bank, GA (last). Talbot State Bank is operating under an enforcement action that restricts its use of both brokered and internet deposits.

Because they don’t facilitate the placement of deposits (nor do they receive compensation from the institutions they list) listing service deposits are more difficult to track. As a result, deposits gained from listing services are estimates only. Listing service deposits are also being reevaluated through the new proposed rule (see last week’s article). Some banks that are not allowed to use brokers instead use listing services as an alternate source of funding. Bauer is the ONLY listing service that self-limits the banks it lists to “Well-Capitalized” and “Well-Rated”… Because while they may be federally-insured, not all banks are credit-worthy.

1 comment on “Brokered Deposits – “It’s Complicated””

Comments are closed.