Despite much negative press to the contrary, most commercial loans are still holding up quite well.

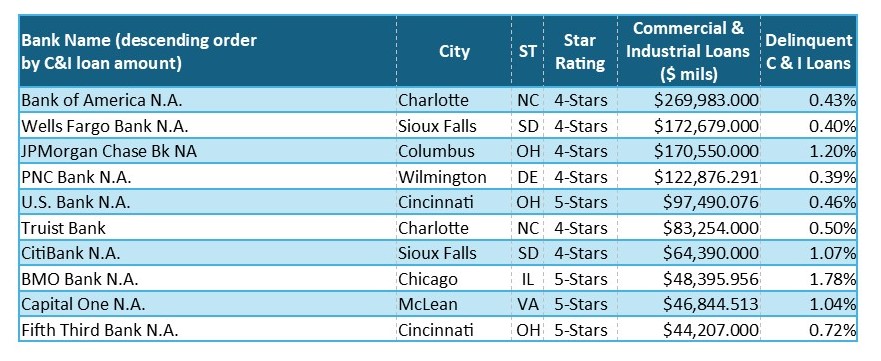

The 10 banks with the highest amount outstanding in C&I loans control 45% of the industry's C&I and are all rated at least 4-Stars by Bauer.

However, some of the smaller players, in C&I as well as CRE lending, are definitely worth watching.

Commercial Loans (Not) as Bad as They Appear

There has been much negative press regarding commercial real estate loans and commercial and industrial loans, but are they really as bad as advertised?

Let’s start by stating that these are two similar, but different, animals. Both are dependent on businesses—large and small companies, and every size in between. Commercial Real Estate (CRE) loans are collateralized by commercial real estate (like a home loan). If they default, the bank can repossess the property and sell it.

Commercial and Industrial (C&I) loans may or may not have collateral. If they do, the terms will be more favorable for the borrower, but depending on the collateral, it may not be as easy to turn around and sell in the event of a default. Of the $2.5 trillion outstanding in C&I loans, 45% is at the 10 banks listed below. As you see, delinquencies are not a “major” problem at most of these heavy hitters (most report delinquencies of well below 1%).

The most prominent exception is the 5-Star BMO Bank, N.A., Chicago, IL which, if you recall, acquired Bank of the West, a $92 billion asset California bank, in February 2023 (JRN 41:02,19). BMO Bank is now the 13th largest U.S. bank. C&I loans account for almost one-third of its loans and, even though 1.78% of its C&I loans are delinquent, its total nonperforming loans as a percent of assets is just 0.66%.

These are the banks where commercial loans may actually be as bad as they appear. Let’s take a closer look. We examined two of them last October as well (JRN 40:41).

The first, 1-Star BancCentral N.A., Alva, OK has lost a star since that October report. It has also been on Bauer Troubled and Problematic Bank Report for the past three years and has been operating under a Cease and Desist Order since 2021. The C&D requires a leverage CR of 9%. For four quarters it was able to achieve that goal, but slipped to 8.98% at year-end then stumbled all the way to 8.35% in the first quarter.

Sadly, that doesn’t even begin to tell its story. Delinquencies are plaguing BancCentral. Nonperforming loans to assets are 12.3% and to net worth they are 272%. Delinquent loans are 25% of total loans and its Bauer’s Adjusted CR is negative (–2.88). What’s more, BancCentral has not posted a profit in the past six quarters.

A new president and CEO, Taylor Horst, was brought in last October to try to turn things around and for a moment there was a glimmer of hope. We tried to take a sneak peak at second quarter financial data, but it is not yet available. So, only time will tell if that glimmer will turn into a flame.

The financial condition of 3½-Star Solon State Bank, Solon, IA is nowhere as dire as that of BancCentral. It continues to be very well capitalized with a leverage CR of 22%. Its loan volume grew over 14% during the 12 months ending March 31, 2024 and it remains profitable. However, while there has been improvement in loan quality since JRN 40:41, nearly 12% of Solon State Bank’s commercial loans are delinquent and its nonperforming asset to total asset ratio is still 7.5%.

The other one we will examine today is 4-Star Emigrant Bank, Miami, FL, which has the highest dollar volume of C&I loans of any bank listed on page 5 ($2.408 billion, over half of its entire loan portfolio). Emigrant Bank has an unusual story.

Emigrant Bank was originally established in NYC in 1850 by a group of Irish immigrants. Its FDIC Certificate # was 12054 and over the years it grew to be a multi-billion bank. In October 2023, Emigrant Bank acquired Plus International Bank, a $52 million bank in Miami. With that purchase, Emigrant also acquired Plus International’s FDIC #57083 and moved its headquarters from NYC to Miami. While this new Emigrant does have hefty delinquencies, it also has robust capital levels. Its leverage CR is 22.9%, its risk-based CR is 21.7% and its Bauer’s Adjusted is 19.6%.

That removes any concern there may have been regarding BMO’s C&I. In fact, we are not concerned with any of the ten listed here.

That being said, there are 50 banks with commercial loans (both CRE and C&I combined) that are less benign. They have the following things in common:

- Commercial Loans (including C&I, CRE and multi-family real estate) make up over 50% of their total respective loan portfolios;

- When combined, delinquencies in these commercial loan categories exceed 3% of the value of those combined loans;

- They are rated less than 5-Stars; and

- They each have assets of at least $50 million. (We eliminated four banks with less than $50 million in assets.)