U.S. banks charged off $12.8 billion in loans in the second quarter 2019. That’s up $1.1 billion or 9.3% from a year earlier. The majority of that increase was due to uncollectible credit card loans, which were up $669.4 million or 8.3%.

After charging off all those bad loans, the noncurrent rate went down 4.8% (surprise, surprise). Almost three-quarters of all U.S. banks also reported increased loan balances during the quarter. And while all major loan categories rose, consumer loans led the way, increasing by $42.2 billion or 2.5%.

In fact, over the 12 month period ending June 30, 2019, consumer loans increased 5.4% at the nation’s banks. The credit card loan portion increase was nearly identical at 5.3%. If we look at just community banks though, those numbers change dramatically.

Consumer loans at community banks increased just 3.8% over the same 12 month period. Their credit card lending, however, was up 7.5%. This is NOT because more community banks are offering credit cards. Rather because credit card balances are creeping up.

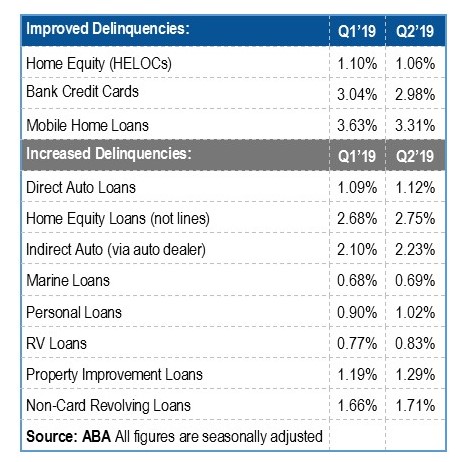

Knowing that, we read with interest the American Bankers Association (ABA) second quarter Consumer Credit Delinquency Bulletin, which was released last week. The ABA breaks consumer loan delinquencies into 11 categories. The credit card loan category was one of just three that showed improvement.

ABA Chief Economist, James Chessen, expects current delinquent loan trends to continue. Sorry to say, but we are inclined to believe he might be right.

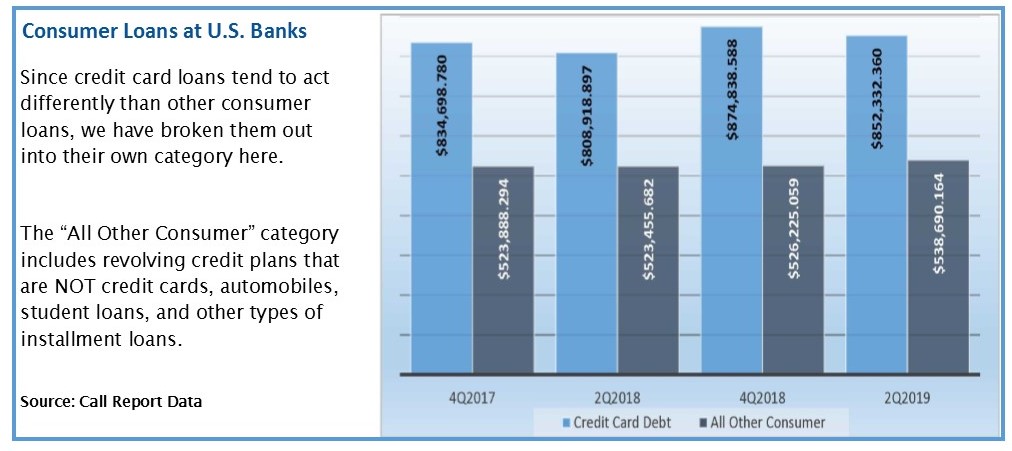

Credit card bank debt (pictured below) tends to peak in the fourth quarter, most likely as a result of Holiday shopping. As consumers pay down this debt, the credit card balances decline. If that were the entire story, the cycle would not be concerning. However, not only are the peaks getting higher, so are the lows. In fact, credit card balances in June 2019 were higher than December of 2017.

Other consumer debt at the nation’s banks (also pictured below), which includes other revolving debt (aside from credit cards) and auto loans, is also beginning to trend up. Upon closer inspection, this increase can be attributed solely to auto loans, which were up 3.55% in the 12 months ended June 30, 2019. Other revolving debt actually did decrease, almost 1% from June 2018 to June 2019.