After the three fairly large and very public bank failures earlier this year, we heard much anecdotal evidence that deposits fled from banks to credit unions.

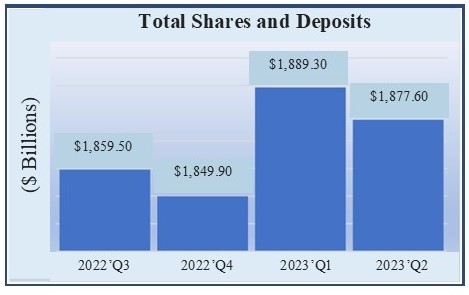

Credit Union deposits did, indeed grow by 2.13% in the first quarter.

Bauer's LLAMAS Report Bundle provides a 5 quarters of data side-by-side to easily track a credit union's growth along with graphs and ratios comparing it to its peers.

Credit Union Share (Deposit) Growth

After the three fairly large and very public bank failures earlier this year, we heard much anecdotal evidence that deposits fled from banks to credit unions. So, while we measured bank growth last week in assets, this week we are measuring credit union growth in shares/deposits.

Credit Union deposits did, indeed grow by 2.13% in the first quarter. They don’t appear to be very sticky, though. It appears some of those new deposits are already fleeing.

The 50 credit unions on page 5 each reported more than 25% year-over year deposit growth based on June 30, 2023 data. They are also all well-established (opened prior to 2013) and are all rated by BauerFinancial (eg: federally insured with more than $1.5 million in assets).

The credit union with the most share/deposit growth during the 12 months ended June 30, 2023 was by far 4-Star LOC Credit Union, Farmington, MI. Or was it?

Actually, 4-Star MemberFocus Community C.U., Dearborn, MI (with assets of $133 million, shares/deposits of $126 million and 8,200 members) and the much larger LOC FCU (with assets of $322 million, shares/deposits of $307 million and 22,100 members) hatched a plan in 2001.

The smaller MembersFocus, would acquire the larger LOC FCU. The new (now state) credit union would keep MembersFocus’ charter, but would then change the name to LOC Credit Unions (losing the “Federal” part).

Completed on July 1, 2022, the new LOC C.U. was opened to the entire state of Michigan. It ended the second quarter ’23 with assets of $446 million, deposits of $414 million and 28,000 members. So, the 228% year-over-year growth refers to MembersFocus’ growth, but with a name change thrown in.

5-Star Cent Credit Union, Mason City, IA is very easy to track. At the end of 2022, Cent CU reported total assets of $73.220 million and total deposits of $64.056 million.

Then, on January 1, 2023, Cent CU acquired 3-Star N.W. Iowa C.U., Le Mars, IA. Adding N.W. Iowa C.U.’s $87.334 million in assets and deposits of $78.285 million, gets you very close to what Cent C.U. reported at the end of March. As with most mergers, there was a little attrition after the transaction was completed, but Cent, the surviving C.U., has more than doubled its deposits.

Let’s head up to New England, where credit unions first got their start in this country with St. Mary’s Cooperative Credit Association, in Manchester, NH. One of the larger credit union mergers that we’ve seen happened just a few miles south of there in Massachusetts.

The acquirer, 4-Star Merrimack Valley Credit Union, Lawrence, MA, with $1.371 billion in assets acquired 5-Star RTN Federal CU, Waltham, MA with $1.022 billion in assets on June 1, 2023. The combined credit union, with $2.3 billion in assets, is the fifth largest credit union in the Bay State and among the largest 200 credit unions nationwide.

This is Merrimack Valley’s fifth credit union acquisition since 2012. RTN, originally Raytheon Emp. CU, was no stranger to acquisitions and mergers either, with even more transactions under its belt. The combination of the two was seamless. The only problem now is that most former RTN members are actually south of the Merrimack Valley. A new name will be rolled out in 2024.

In the meantime, Merrimack Valley CU’s membership has grown by more than 50% and its deposits over 78% since last June. Yet, we have still seen no evidence of deposits migrating from banks.

Maybe we’ll have better luck in California. That’s where the failed Silicon Valley Bank and First Republic Bank were headquartered. But no, only one California credit union made our list and it’s 5-Star Fresno Grangers FCU, Fresno, CA, a small ($33 million asset) local credit union. It clearly did not enjoy a windfall from the bank crisis.

Perhaps we are looking at this the wrong way. Credit unions, unlike banks, have fields of membership. Not everyone can open an account (unless it’s a minority or limited income credit union, but that’s a story for another day). Perhaps there was an inflow into the CU system, but it was spread widely across the industry.

If that’s the case, then 5-Star Navy FCU, Vienna, VA, as the largest and widest ranging U.S. credit union, will shed some light. In the 12 month period, Navy FCU gained 4.6% in assets. Its deposits grew slightly more at a rate of 6.85%. Most of that deposit growth was, in fact, during the first quarter ’23, when people were scrambling for safety.

It is by no means a definitive answer, but it does appear people may have moved deposits from their bank to their credit union resulting in an industrywide increase.