The Federal Reserve’s Beige Book is a survey of opinions. While qualitative in nature, those surveyed do tend to have their fingers on the pulse of their part of the country. The latest Beige Book was based on information collected before January 8th. The partial government shutdown was well underway, but at the time of these surveys, respondents didn’t know that this shutdown would end up being the longest in U.S. History.

Most regions reported a modest increase in consumer spending. Consumer confidence remained elevated in most areas as well. The Boston Region expressed some concern over the long-term effects of increased tariffs, but only the Chicago Region seemed remotely concerned about the partial government shutdown.

Encouraged by their regulators, many small banks and credit unions are finding ways to work together with government employees to get them through this rough patch and some big banks are as well. As for the others, Sen. Warren (D-MA) has requested details on what they will offer by Monday (January 21st, which also happens to be Martin Luther King Jr. Day, a National Holiday).

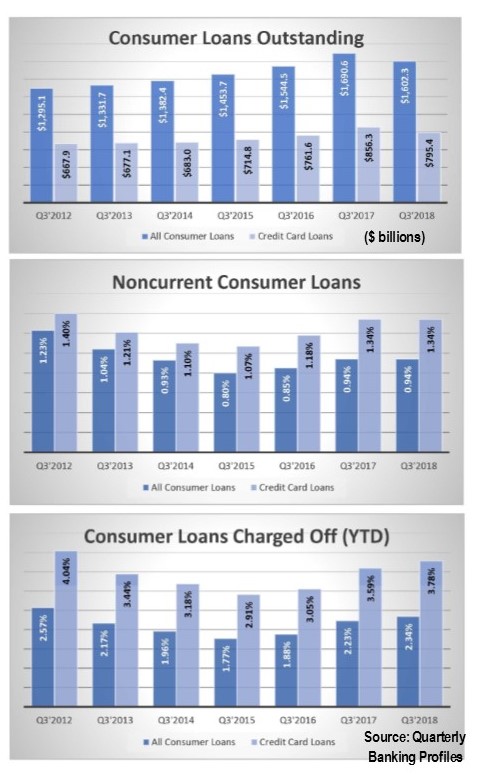

In addition to helping their customers, though, these financial institutions also have to protect themselves. The first chart on page 2 shows that consumer debt at the nation’s banks was just below $1.7 trillion at September 30, 2018. But that’s just at banks.

According to the Federal Reserve Bank of New York, total household debt (banks, credit unions, finance companies, mortgage companies, etc.) rose for the 17th consecutive quarter to a record high of $13.5 trillion. That’s $837 billion higher than the previous peak which was exactly ten years earlier (Q3’2008).

The percent of those loans that are noncurrent is also on the rise, with student loans faltering the most followed by credit card loans. The majority of student loans are not granted by banks, but credit cards are. According to the FDIC Quarterly Banking Profile, which tracks all FDIC-insured banks, the percent of noncurrent consumer loans (delinquent 90 days or more) jumped from 0.88% to 0.94% during the third quarter 2018. However, it was on par with third quarter of the previous year. (The numbers were similar for the credit card subset.)

The percent of charged-off consumer loans, on the other hand, has been increasing for the past three years. Consumer loan charge-offs for the first nine months of 2018 were 2.34% while charged-off credit cards accounted for 3.78% of total bank credit card loans. That’s up from 2.23% and 3.59%, respectively, a year earlier and 1.85% and 3.05% two years earlier.

Anecdotal evidence suggests that bankers are tightening their underwriting standards to reign-in these increases. This, combined with increases in interest rates and insecurity about the economy could dampen loan demand and the economy as a whole, in the coming months.

The banks on page 7 have the highest percent of consumer loans 90 days or more past due as long as the bank’s consumer loans account for at least 20% of total loans.