Have you ever wondered why we list the annual percentage yield (APY) on our consumer CD rate page, but we list the annual percentage rate (APR) on our corporate CD rate page, Jumbo Rate News? Perhaps not. Perhaps you never even noticed. And, even if you did notice, you probably didn’t give it much thought.

It was close to 30 years ago now (1991 to be precise), that the Truth in Savings Act (TISA) was passed. TISA was designed to provide consumers with apples to apples comparisons on savings vehicles. Until then, some banks would quote APR while other quoted APY which made comparison shopping very difficult.

The annual percentage rate (APR) is a straight percentage that does not include any compounding of interest. Most banks do compound interest, but not all. And on top of that, those that do vary on the frequency of that compounding. The annual percentage yield (APY) takes the compounding into consideration. Compounding increases the principal on which you will earn interest in the future.

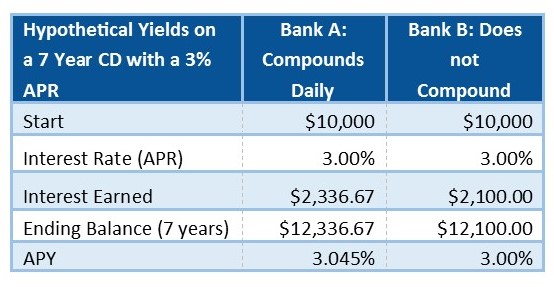

For a simple demonstration, let’s say you have $10,000 and you want to open a certificate of deposit (CD). Bank A and Bank B both have APRs of 3% for a 7 year term. However, Bank A compounds interest every day. So, while the interest rate remains the same, you will earn more as evidenced here:

TISA requires all banks to use APY in their advertising to consumers. It also requires the banks to include a statement saying that the APY assumes all principal and interest will be left on deposit for the full duration of the CD.

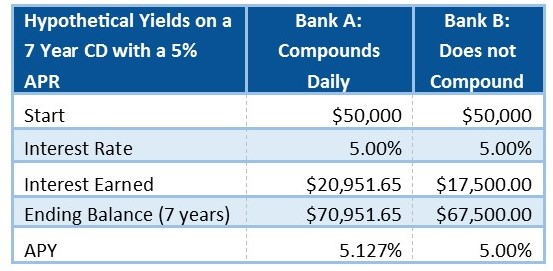

The example above is fairly small so the variance is not that great, but the higher the deposit amount and/or rate, the more variance you will see between Bank A and Bank B. Like below:

Because corporate depositors are more likely to request monthly interest payouts, they were excluded from TISA. And rightly so. The APY means nothing if you do not leave all of your principal and interest on deposit for the entire length of the term.

So now you see how you can earn more on your CD by looking at APY instead of APR, but the title promises you can save thousands. It’s true. Because these same principles apply to loans. Particularly if you have credit card debt that is not paid off monthly, you are paying compound interest. You could be paying a lot more than you bargained for if you did not compare APYs on any loan. And yes, it could be thousands.