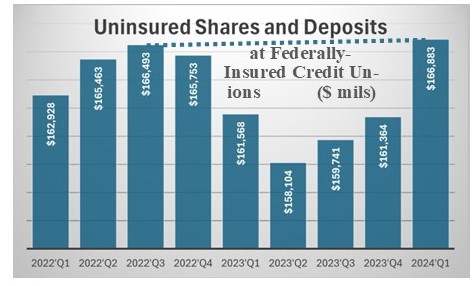

Federally-Insured U.S. Credit Unions hold roughly $167 billion dollars in uninsured shares or deposits. About 3/4s of the industry has some amount of uninsured deposits on their books.

In addition to looking at key metrics from 1st quarter 2024 credit union financial reports, in this week's issue of Jumbo Rate News, we also look at a number of credit unions that are less than “Well Capitalized” by regulatory standards, and also have a significant amount of uninsured deposits on their books.

Many of the credit unions listed can also be found on Bauer’s Troubled and Problematic C.U. Report which includes all credit unions rated 2-stars or less as well as credit unions that are not rated (N.R.) but undercapitalized.

New C.U. Star-Ratings and Data Now Available

Let’s start with the good news. Total assets at our nation’s federally-insured C.U.s increased 4.4% during the 12 months ending March 31, 2024. That calculates to $96 billion for a total of $2.31 trillion.

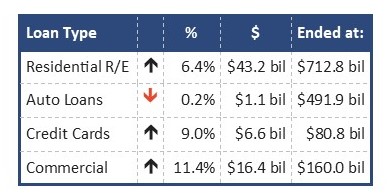

Total loans, the largest segment of assets, grew 4.6%, or $70.7 billion ending the first quarter 2024 at $1.6 trillion. The average outstanding loan balance of $18,062 was up 4.3% from the previous first quarter. Major loan categories include:

Overall, credit quality is still quite good, even though the delinquency rate increased 25 basis points (bps) from a year earlier. At 78 bps, it is still well below the 1% mark. That is, until you look at credit cards. Credit card delinquencies rose 54 bps over the year ending the first quarter 2024 at 2.02%.

This rate is down, however, from year-end ’23 when the credit card delinquency rate was 2.11%. That could be due to an increase in charge-offs which went from $7.9 billion in the first quarter of 2023 to $9.5 billion in Q4 (just over 20%). In the first quarter of this year, charge-offs jumped all the way up to $12.9 billion (another 36% jump). As a percent of total credit card loans, charge-offs represent roughly 0.8%.

As a result of the deterioration in loan quality, provisions for loan losses increased 45.8% in the most recent four quarters. This provisioning has positioned most credit unions quite well in the event of a worst-case scenario.

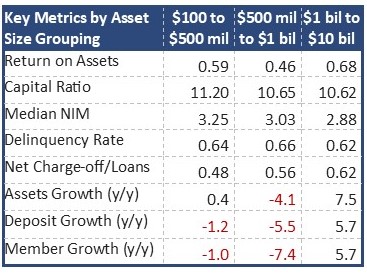

Fewer than 10% of the nation’s 4,572 federally-insured credit unions posted all around growth in the 12-months ending March 31, 2024. These are the 443 largest CUs; each has assets that exceed $1 billion.

The other 4,129 credit unions (the 90% with assets less than $1 billion) lost deposits and members. All but one subsection also lost assets. The group with assets between $100 and $500 million gained 0.4% in assets.

Interestingly, this group of 1,069 credit unions surpassed the next larger group—the 274 credit unions with assets between $500 million and $1 billion—in most key metrics.

All size groupings with assets less than $100 million (60% of the total) lost assets, deposits and members. The smallest group, however, somehow managed to grow loans.

There are currently 93 C.U.s included on Bauer’s Troubled and Problematic C.U. Report (i.e. rated 2-stars or less OR not rated (N.R.) but undercapitalized). Seventy-nine are less than “Well-Capitalized” by regulatory standards; 23 are less than “Adequate”.

About 70% of these subpar C.U.s are carrying uninsured deposits on their books. (There is also a de novo, established in 2021, with $1.794 million in uninsured deposits. That institution is N.R. Unity of Eatonville FCU, Eatonville, FL.) Aside from Unity, the 50 with the largest amount of uninsured shares/deposits can be found on page 5. Three have more than $100 million at risk. They are:

3-star Collins Community Credit Union, Cedar Rapids, IA, which was on this list last November (JRN 40:44) as well. Instead of decreasing uninsured shares, they increased over 30%-from $120.878 million to $158.259 million in the three quarters since.

3-Star Dort Financial Credit Union, Grand Blanc, MI is in a similar situation, except it was its acquisition of the $514 million Flagler Bank, West Palm Beach, FL in December 2023 (JRN 41:17) that caused Dort Financial C.U. to lose its “Well-Capitalized” status. Its uninsured deposits grew 27%-from $87.5 million to over $111 million in six months.

2-Star True Sky Federal Credit Union, Oklahoma City, OK has a history of carrying some amount of uninsured shares/deposits on its books. In the past 2 years that amount has ranged from about $93 million to over $217 million. It wasn’t until year-end 2023, however, that True Sky lost its “Well-Capitalized” designation adding it to this list. It can now also be found on Bauer’s Troubled and Problematic Credit Union Report.

Consumers panicked last spring with three high-profile bank failures. Uninsured shares and deposits at both credit unions and banks decreased as a result. Deposits were transferred quickly for maximum deposit insurance coverage. It seems the scare is wearing-off. Uninsured credit union deposits have now surpassed their previous high.