Wells Fargo has been the poster child for years now for charging excessive fees. The bank is now in the hunt for its third CEO in as many years with both regulators and Congress keeping a watchful eye. So much so, in fact, they are likely to greatly narrow the field of potential replacements.

In another recent development, the Consumer Financial Protection Bureau (CFPB) announced it is conducting a review to determine the impact of Regulation E on small entities. Regulation E was amended in 2009 with the intention of empowering consumers in matters of overdraft fees, ATM charges and a number of other transactions collectively referred to as Electronic Fund Transfers.

Anyone who has been to an ATM in the past decade has been notified of the charges they will incur (if any) and given the option to cancel the transaction and avoid the charge. Reg. E’s amendment also required customers to opt-in for the “privilege” of being allowed to overdraw their account and incurring an associated fee (JRN 30:23). From the beginning, there were concerns that this could disproportionately harm smaller institutions.

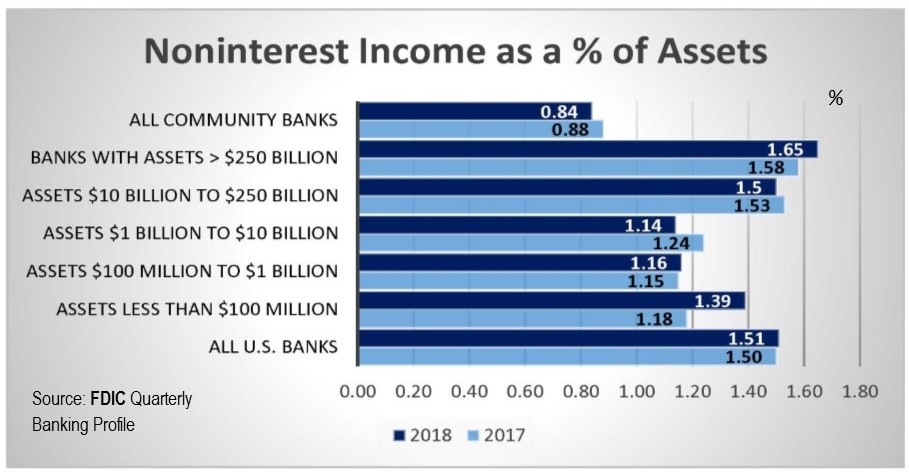

All banks require a certain amount of noninterest income. Bigger banks have other avenues from which to earn it (from trading revenue to sales and servicing of mutual funds or annuities to brokerage activities).

Smaller banks typically rely more on traditional banking—savings and lending. To illustrate community banks’ dependence on these fees, compare the following:

Wells Fargo Bank earned $25.559 billion in total noninterest income in 2018. Of that, only 20% ($5.145 billion) was from service charges on domestic deposit accounts.

Conversely, noninterest income at FSNB, NA (the first bank listed on page 7) totaled $56.222 million at year-end 2018. Of that, 86% ($48.294 million) was derived from service fees. FSNB may not be a typical community bank, so we looked at #2, First National Bank Texas, which earned over half ($147.126 million) of its noninterest income ($281.160 million) from service charges on deposit accounts.

The graph below compares 2017 and 2018 total noninterest income at various subgroups of banks. Keep in mind, this is all noninterest income, but it drives home the point that community banks are different animals than the Big Banks and should be treated differently by regulators.

We are not suggesting the Reg E should be repealed. Consumers should have the right to choose whether or not they want to pay for certain courtesies. But we are pleased to see regulators taking the time to look at how some regulations can disproportionately (and negatively) affect community banks. That will become even more important if and when the Fed decides to cut rates.

Comments will be accepted for 45 days after publication in the Federal Register, which should be soon. Visit the CFPB for more information.

1 comment on “Protect Consumers, Don’t Harm Community Banks”

Comments are closed.