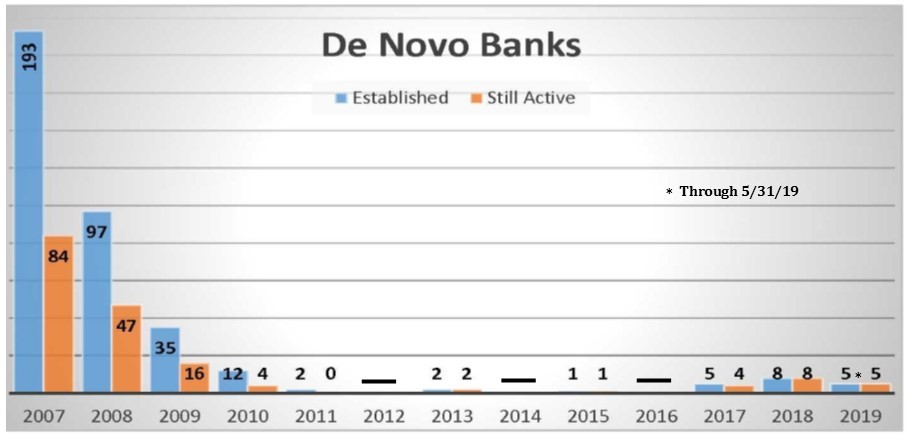

Two new banks reported 1st quarter 2019 financial data for the first time and several more are in varying stages of the de novo process (see page 7).

Established on 12/31/2018, 3½-Star Generations Commercial Bank, Seneca Falls, NY was the last of eight de novo banks to debut in 2018. While that just leaves one actual new bank during the first quarter, 3½-Star Watermark Bank, Oklahoma City, the second quarter has already produced five more.

Another six have been approved and expect to be up and running before year-end and ten are awaiting FDIC deposit insurance approval. That puts 2019 on track to more than double 2018’s number of de novo banks.

Submitting an application to start a de novo bank doesn’t always mean it will be approved. While the FDIC has tried to help the process along, it is not the only regulator involved. State banking regulators have to be onboard if the de novo wishes to be state-chartered while the OCC must approve all national charters. Either way, a number of matters must be scrutinized including: the business model, ownership structure, affiliate relationships, management & board members, source and level of capital and projections for the first 3 years. And that’s just a start.

Organizers are encouraged to solicit feedback from the FDIC and hold a pre-filing meeting to review their proposal prior to submitting deposit-insurance applications. In spite of that, two entities that received provisional FDIC approval last December have since withdrawn their applications. One was to be called Spirit Community Bank, Statesville, NC. The other Tarpon Coast Bank, Port Charlotte, FL.

While we can’t say for sure why the applications were pulled, the word “provisional” must not be overlooked. (Note that the column heading on the page 7 chart reads “FDIC Insurance Approved”, it should actually read “Provisional FDIC Insurance Approval”.) In addition to stipulating the minimum initial capital required to open the new bank and a minimum leverage ratio, public comment is solicited on any proposed bank as is CRA approval.

If any of these prerequisites goes sour, the application is apt to be pulled. Or, a better deal might just happen along. That seems to be the case with the would-be Dogwood State Bank that never was in Raleigh, NC.

Organizers applied with the state of North Carolina and the FDIC last year and received provisional approval to open Dogwood State Bank. They pulled the plug on that plan a short four months ago electing to put their money towards recapitalizing an existing community bank: 5-Star Sound Bank, Morehead City, NC. The $100 million capital injection, which we will see in Sound Bank’s second quarter call report, will be used to “grow the franchise into a high performing, statewide North Carolina community bank”.

The pending merger between BB&T, Winston-Salem, NC and Suntrust Bank, Atlanta, GA may seem to make the Southeast Region a prime target for new community banks. But that’s just the latest blow to the area. The Great Recession hit that area particularly hard. Georgia lost more than 90 community banks between 2007 and 2016 and Florida lost over 70. While those numbers are daunting, there are currently 168 and 114 banks, respectively, that call these states home.

Arizona lost half of its community banks. It only had 30 to begin with but is down to 15 local. So, while we are happy to have all de novos, we are particularly pleased to see reports of five de novo applications in the Grand Canyon State.