Since the end of 2019 (before the pandemic recession), household debt has increased by $3.7 trillion (28.4%).

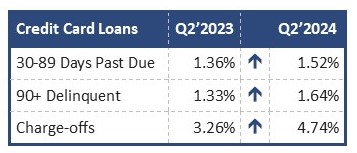

Even more disturbing is how much of this debt is beginning to falter. Credit card delinquencies are flirting with the 11% mark for the first time in 12 years.

Five big banks (listed below) account for more than half of total bank credit card debt. While they continue to perform well, 50 others that are headed in the wrong direction can be found on page 5 of this week's issue of Jumbo Rate News.

Total Household Debt Increased $109 Billion in Q2

In the second quarter of 2024, total household debt increased by $109 billion. Since the end of 2019 (before the pandemic recession), it has increased by $3.7 trillion! It’s no wonder we’re feeling pinched. In the twelve months ended June 30th:

The second quarter numbers may seem mild when compared to year-over year, but consumer debt continues to climb and is 28.4% higher than 5 years ago. The credit card debt, in particular, gives a clear indication that people are having trouble making ends meet. Even more disturbing is how much of this debt is beginning to falter. Credit card delinquencies are flirting with 11% for the first time since 2012 (12 years ago). Even short-term credit card past-dues (30 day+) have surpassed 9%. The first quarter 2011 was the last time that happened. Source: Federal Reserve Bank of New York, Household Debt and Credit Report (analysis based on New York Fed Consumer Credit Panel and Equifax data).

The second quarter numbers may seem mild when compared to year-over year, but consumer debt continues to climb and is 28.4% higher than 5 years ago. The credit card debt, in particular, gives a clear indication that people are having trouble making ends meet. Even more disturbing is how much of this debt is beginning to falter. Credit card delinquencies are flirting with 11% for the first time since 2012 (12 years ago). Even short-term credit card past-dues (30 day+) have surpassed 9%. The first quarter 2011 was the last time that happened. Source: Federal Reserve Bank of New York, Household Debt and Credit Report (analysis based on New York Fed Consumer Credit Panel and Equifax data).

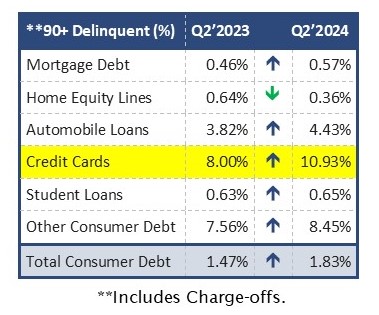

You know what’s happening to your own wallet, but let’s see how these trends are affecting our banks. According to the FDIC’s Quarterly Banking Profile, total consumer loans were up just 1.9%, but credit card loans at U.S. banks were up $77 billion (7.5%) year-over-year. Comparing second quarter 2023 past due credit cards with second quarter 2024, everything is up:

There are some banks that are being hit particularly hard with rising nonperforming credit card loans.

In addition to earning a Bauer rating of 3½-Stars or lower based on June 30, 2024 data, each of the 50 banks listed on page 5 reported year-over-year growth in consumer loans as well as a year-over-year increase in the percentage of those consumer loans that are 90 days+ delinquent. This does not mean they are the worst, but they are definitely heading the wrong direction.

Before we go any further, five big banks account for more than half of total bank credit card debt. They are all performing pretty well. (See below.) Even the two credit card banks (Capital One and Discover) which each reporting total delinquencies excess of 1.70%, have sufficient capital to cushion the blow if forced to write them off.

|

Bank Name |

City |

ST |

Star Rating |

Credit Card Loans ($ mils) | % of Total Bank CC Loans | Delinquent CC Loans ($ mils) | Credit Card Delinq. | Total Delinq. Loans | Leverage Capital Ratio |

Bauer’s Adjusted CR |

| JPMorgan Chase Bank N.A. | Columbus |

OH |

4-Stars | $187,589.000 | 16.98% | $1,980.000 | 1.06% | 0.78% | 8.13% |

7.86% |

| CitiBank N.A. | Sioux Falls |

SD |

4-Stars |

$156,534.000 | 14.17% | $2,420.000 | 1.55% | 0.67% | 8.99% |

8.75% |

| Capital One N.A. | McLean |

VA |

5-Stars |

$133,790.016 | 12.11% | $3,528.317 | 2.64% | 1.79% | 10.55% |

9.44% |

| Discover Bank | Greenwood |

DE |

4-Stars |

$99,914.670 | 9.04% | $1,984.821 | 1.99% | 1.72% | 10.22% |

8.88% |

|

Bank of America N.A. |

Charlotte | NC |

4-Stars |

$99,450.000 | 9.00% | $1,257.000 | 1.26% | 0.74% | 7.63% |

7.34% |

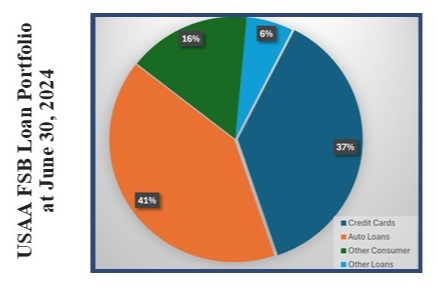

Many of the banks on page 5 also have sizable capital cushions. For example: 3-Star USAA Federal Savings Bank, Phoenix, AZ has a leverage capital ratio (CR) of 8.46%; its Bauer’s Adjusted CR is 8.21%, so it has plenty of cushion. But… during the 12 months ending 6/30/2024, its credit card loans increased 8.17%, from $15.281 million to $16.529 million.

Neither this June 30th nor a year ago, did it report any credit cards that were 90 days past due and still accruing. However, in June 2023, it did have $170 million that was no longer accruing and $99 million that was 30-89 days past due. This June 30th, those numbers were up to $224 million (an increase of $54 million or 32%) and $119 million (an increase of $20 million or 20%), respectively. The vast majority of USAA’s loans are consumer loans. In fact, auto loans and credit cards account for 78% of the total. Its largest pie slice is auto loans which, at least so far, are performing much better than credit cards, in spite of short term past dues creeping up.