Chairman of the Federal Reserve, Jerome Powell, made some poignant remarks in a speech on Wednesday. What we found particularly disheartening was that: People who had a job in February and whose annual household income was less than $40,000 stood a 40% chance of losing a job in March.

Some of those people will find other jobs, but he went on to state that longer stretches of unemployment, for those who can't find another job, can damage or even end a career. This inevitably leaves families in greater debt and with less ability to pay that debt off.

Mr. Powell has assured us that the Fed, with the help of the Treasury, will do whatever it can to avoid these outcomes, but he reminds us that the Fed's powers are limited and that this is something never seen before. There is no playbook.

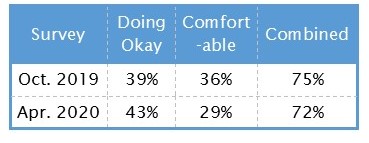

On Thursday, the Fed followed that up with results of a well-being survey it had started last fall with a follow-up this April. Last October, among over 12,000 U.S. adults surveyed, 75% said they were at a minimum "doing okay". Of those, 36% considered themselves to be "living comfortably".

Six months later, a smaller follow-up survey of just over 1,000 indicates a definite downward trend.

Bear in mind, the unemployment rate last October (2019) was 3.6%. By this March, unemployment was heading up, but it had just begun the journey. The unemployment rate of 4.4% for March 2020 was still quite good. It wasn't until April that it really took flight. The April rate of 14.7%, which will be even higher in May, has not yet been factored into the numbers above.

A large number of the unemployed came from furloughs, nine out of ten of which expect to return to their same jobs, eventually. They just don't know when.

Furloughed or not, the longer a person is unemployed, the more likely it is that the household will fall behind on its monthly bills.

As we mentioned last week, when people lose their jobs, they often turn to credit cards to pay for necessities. In that eventuality, credit card loan quality could suffer greatly. We need to keep an eye on any federally-insured institution that could be adversely affected in that eventuality.

Last week we listed 50 banks with high credit card loans on their books at year-end 2019. This week, we are listing the 50 credit unions with the highest percent of loans at 12/31/2019 that were reported as credit cards. While credit unions are less likely than banks to have rewards programs tied to their credit cards, they are more apt to have lower interest rates and fees. That makes them an attractive option for many people.

However, since credit unions (as a rule) tend to be smaller than banks, it takes fewer bad loans to have a negative impact. At the same time, if an institution has a high percent of loans concentrated in credit cards and its field of membership takes a financial hit or has widespread layoffs, the repercussions could be swift and painful.

For example, the end of 2019, 5-Star Pepco FCU, Washington, DC had $8.162 million in total loans. Over 42.4% of them ($3.465 mill) were credit card loans. And the quality, while not perfect, was quite good.

Out of 772 total credit card loans, 13 were more than 59 days delinquent for a total of $80,092. Eight more totaling $47,147 were 30-59 days past due. The total $127,239 past due to any degree represented 3.7% of all credit card loans.

A preliminary look at Pepco FCU's March 31, 2020 shows six fewer credit card loans and a lower outstanding (down from $3.465 million to $3.263 million). Loans delinquent 60 days or more delinquent, however increased from 13 to 15 and now totaled $81.752. Those 30-59 days past due grew from eight to 35!

That means, in the first quarter, which we have already conceded is just the tip of the iceberg, its past due loans (30 days or more) grew in number from 21 to 50 and in dollar amount from $127,239 (3.7%) to $300,524 (9.2%). March data will be interesting.