The Fed’s latest dot plot suggests we could end 2025 with the Fed Funds rate under 4%. You guessed it. CD rates will closely follow. Forecasts beyond 1 year are less reliable, but still suggest that more easing will be forthcoming.

A lot can happen in 12 months, though. Just look at the upward change in projected inflation in just two months (between September and December 2024). If that remains elevated, so too, will the Fed Funds Rate.

What Will Happen to CD Rates in 2025?

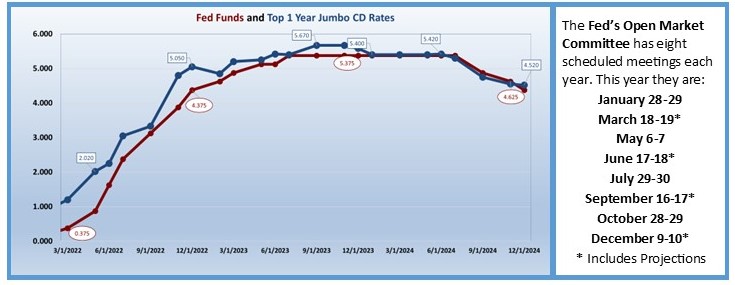

After two full years of near zero interest rates (when the Fed Funds target was between zero and 0.25%-March 18, 2020 to March 16, 2022) the Federal Reserve’s Open Market Committee, (FOMC) decided it was time to start tightening.

It began slowly, with a 25 basis point increase on March 16, 2022, but it continued. Subsequent increases would be made in each of the FOMC’s following nine meetings. They ranged from 25 basis points to 75 basis points each.

Finally, a pause at the June 14, 2023 meeting, just to see how things were progressing. Then we saw one more increase in July before the FOMC was content to stay put for a while. The Fed Funds target was between 5.25% and 5.5%.

For the next eight meetings (a full year), the Fed Funds rate remained unchanged. That brought us to September 18, 2024 and a 50 basis point cut in the Fed Funds rate, followed by two more quarter point cuts before 2024 closed out.

The chart below represents these changes in the Fed Funds target rate (red oval) along with the top 1 year Jumbo CD rate from Jumbo Rate News (blue rectangle). You can see as rates climb, the Jumbo CD rate is slightly ahead of the Fed Funds rate, but as they come down, they are more in alignment. That will be important to remember as we look forward to 2025.

The Fed’s latest dot plot suggests we could end 2025 with the Fed Funds rate under 4%. You guessed it. CD rates will closely follow. Forecasts beyond 1 year are less reliable, but still suggest that more easing will be forthcoming. The first meeting of 2025 is scheduled to wrap-up on January 29th, just nine days after inauguration day. We expect nothing will change then. The following meeting, and the first with new projections, is March 19th.

If inflation continues to come in between 2.5% and 3%, we’ll expect another pass at that meeting too. A lot can happen in three months, though, as we saw with the changes in the projections between the September and December 2024 meetings. In September, the committee was projecting 2025 inflation to be between 2.1% and 2.2%. By December, those predictions were up to 2.5%. The higher that is (all other things equal) the longer we will have higher interest rates.

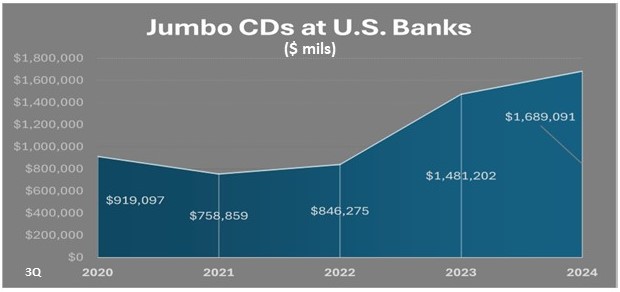

Bankers, in general, would prefer lower rates. They pay less for deposits and attract more loans. Yet, in the past two years, since rates started heading up, Jumbo CD growth at our nation’s banks has far outpaced total deposit growth. In fact, during calendar 2022, when rates went up 4.25%, jumbo CD balances grew 21.8% while total deposits were down 2.5%. That leads us to the 50 banks listed on page 5.

They all have these four commonalities:

1) They each had more than 200% growth in their Jumbo CD deposits during the 12-month period ended September 30, 2024;

2) They each ended the third quarter 2024 with a Jumbo CD liability of at least $10 million;

3) They are all recommended by Bauer (i.e. rated 5-Stars or 4-Stars); and

4) They are all community banks.

Some of the banks listed on page 5 are JRN listees, like 5-Star Community Savings, Caldwell, OH. Community SB has used those new deposits to increase its residential real estate loan portfolio. Just two years ago, Community SB had $30.145 million in single family home loans. That represented about three-quarters of its entire portfolio. Today, residential real estate loans top $186 million and represent almost 97% of total loans. That is how you make lemonade from lemons.

Others, like 5-Star First Security Trust & Savings Bank, Elmwood Park, IL, only open new accounts in their branch offices. While you won’t find these banks listed on our rate pages, if you live near any of them, you could always stop in. While increasing its Jumbo CD liability by over 300%, First Security T&SB’s total deposits did not grow much at all. Deposits simply shifted from non-interest bearing accounts or low-interest accounts into the higher rate CDs. That, we’ll call a missed opportunity. You can’t win them all.