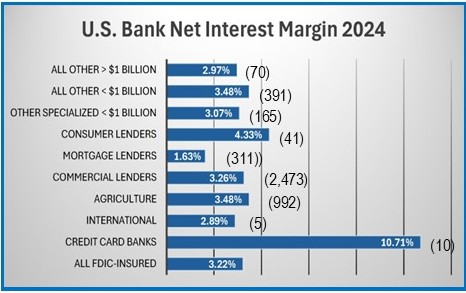

The aggregate net interest margin (or NIM, the difference between interest income generated and interest paid out) at our nation's banks was 3.22% at year-end 2024. This number can vary a lot depending on how big the bank is and what type of loans it specializes in.

As a rule, banks that specialize in credit cards have higher NIMs than other banks. (The aggregate NIM for the ten credit card banks at year-end 2024 was a very impressive 10.71%.)

How can a bank manage to report a NIM of 118%? Continue reading to find out.

When a Bank’s Interest Margin is Too Big

Four weeks ago, we reported that the aggregate banking industry’s net interest margin (NIM) at the end of 2024 was 3.22% (JRN 42:09). We also mentioned that the NIM was close to or above 3.5% for all asset size groups except the largest (i.e. the 14 banks with assets exceeding $250 billion). It is worth reiterating that those 14 banks deal with volumes that allow them to charge lower interest rates on loans; they typically pay lower interest on deposits as well. Smaller banks do not have that luxury.

They can get creative, maybe too creative. A $137 million asset community bank had the highest NIM of all U.S. banks at year-end 2024. 5-Star TBO Bank, Orrick, MO (10597) (f/k/a The Bank of Orrick), had a NIM exceeding 118%!

To see how this was made possible, we have to backtrack a few years. At the end of 2021, The Bank of Orrick reported total assets of just $43.6 million and capital of just $3.4 million. Its NIM was a paltry 2.3%. The bank was ripe for a take-over, and would-be acquirers took notice.

A very high-profile deal was denied by the FDIC in 2022, making even more people take notice. Northeast Kansas Bancshares, Inc., Overland Park, KS, was the fastest to step in to acquire the majority of the bank’s common stock. That transaction was completed in May (2022).

The following May (2023) another Change of Bank Control Application was submitted and approved and before the close of ’23, Orrick Financial Corporation was established as a second tier bank holding company with the Bank of Orrick under it and Northeast Kansas Bancshares, Inc. above.

Just a month later (Jan 4, 2024), the Federal Register reported that another group was now acting to gain control of both Orrick Financial Corp. holding company and The Bank of Orrick. Meanwhile...

In the midst of all of this, the Better Business Bureau opened a file on a company going by the name Atlas Personal Finance (also known as Atlas by Bank of Orrick). This was in November 2022, after it received dozens of complaints against the company.

The complaints were all similar in nature. People with bad credit took out loans from Atlas, happy that a bank would give them credit (and believing that a bank would be better than a payday lender). They were mistaken. Not only did the customers have no idea what the interest rate on the loan was, these loans did not include any of the usual disclosures we have come to expect on our credit card bills.

The Consumer Financial Protection Bureau (CFPB) also received complaints on Atlas and, based on its research, discovered it was offering a Vault brand name “line of credit” with a 379% APR! Outrageous, yes, yet the CFPB’s hands were tied.

Not only was the rate reportedly undisclosed, so was the information box that tells how long it will take to repay your debt. This so-called “Schumer Box” that we have become accustomed to on credit card statements is not required on general purpose lines of credit. Loophole!

The Bank of Orrick has a consumer lending specialty which is reflected in its loan portfolio, with nearly 80% of its loans going to consumers. It has no credit cards or other revolving credit plans on its books. It does have a small amount of auto loans, but the majority of its consumer loans fall into the “other” category, which includes single payment and installment loans, like those offered by Atlas.

In October 2024, The Bank of Orrick became TBO Bank and Atlas was rolled into it. This is how a small community bank in the heartland was able to grow its NIM to 118%. But, this story is far from over.

On March 19, 2025, the Federal Register announced another group (the Kincaid Family Group of Lenexa, KS) is acquiring voting shares of Northeast Kansas Bancshares, the top-tier holding company. This will also give it voting shares in 4-Star Kendall Bank, Overland Park, KS (16471) as well as Orrick Financial Corp. and TBO Bank.

In addition, as of December 31, 2024, TBO Bank has no loans that are 90 days or more delinquent. However... short-term past dues could become an issue down the road. Remember, TBO Bank’s loans cater to people with poor credit and are largely unsecured.

TBO Bank is one of 41 banks that specialize in consumer lending. The aggregate NIM (4.33%) of these 41 is clearly skewed by TBO Bank. Also of note on the chart below is that none of the International Banks nor the Credit Card Banks are community banks; you will not find them on page 5. (Page 5 lists the 50 “community banks” with the highest NIM.) Of the 70 “all other > $1 billion” in assets, 30 are community banks as are all but 10 “Agriculture Banks”, 26 “Mortgage Lenders” and 10 “Consumer Lenders”.