Not us, say Big Banks, in response to comments by Senator Elizabeth Warren (D-MA) who reportedly called out “giant banks that make billions of dollars in profits and squeeze every last penny out of customers who are struggling”.-American Banker 7/19/21. That was just six days after the same paper reported on several regional (and larger) banks rethinking their overdraft fee policies.

It was a month after we reported that one big bank (4-Star Citibank) was already reigning in those fees (JRN 38:22). While we congratulate Citibank on its progress, we would like to call out another bank: 5-Star FSNB N.A., Lawton, TX, a bank that caters to our armed forces, for having one of the highest service fee ratios in the country at 14.3%.

This is not the first time we’ve called out FSNB for over-charging military personnel (most recently in May 2019 (JRN 36:19)). FSNB’s overdraft protection charges a $20 fee for each item paid. The bank touts this “perk” as a way to avoid merchant charges in the event of an honest mistake or emergency. But the costliest mistake is likely opting-in.

Today we’d like to focus on the other extreme: community banks that reported zero or near zero service charges relative to their transaction (ex: checking) accounts at March 31st. We’ve listed 53 recommended community banks on page 7 (i.e. rated 5-Stars or 4-Stars) that fall into this category. Let’s explore a few of them to see how they make money without charging high fees. Yes, they do make money.

4-Star Cenlar FSB, Trenton, NJ’s call report shows that 99.9% of its loan portfolio is invested in 1-4 family residential property. Cenlar FSB is a thrift, so a high percentage of home loans is expected, but 99.9% is extraordinary in any case.

Born in 1985 from the combination of Centennial S&LA and Larson Mortgage Company, Cenlar FSB considers itself a pioneer in the field of subservicing. It should. It has decades of experience and is the leading mortgage loan subservicing company in the nation. Cenlar makes its money by having 3,700 owner-employees servicing loans for other banks, mortgage companies and credit unions across the country. That’s one way to do it.

5-Star Esquire Bank N.A., Jericho, NY has another way. Esquire, as the name suggests, was built by attorneys for attorneys. Its unique “law firm” banking provides the capital needed for case costs, inventory and technology. While it may not seem like a typical community bank, it is in the sense that it understands intimately, the needs of its community of lawyers. Esquire’s mission is their success. That is the mark of community banking. Niche Banking is a different type of community banking which, in this case, has worked out quite well.

Esquire Bank was established in 2006 in Nassau County New York to fill what it perceived as a void in the nation’s banking system: a dedicated partner that practices the business of law every day. Clearly the vision worked. Today, Esquire Bank is nearing the $1 billon asset mark, and it meets or exceeds its banking peers in areas of Capital, ROA and delinquencies.

Its loan portfolio is comprised primarily of Commercial and Industrial (53%) and Construction and Land Development (35%). That accounts for law firm work and office space primarily. The rest is rounded out by single family residential (6.5%) and consumer (5%). With a 0.325% delinquency to asset ratio, their loans are in quite good shape.

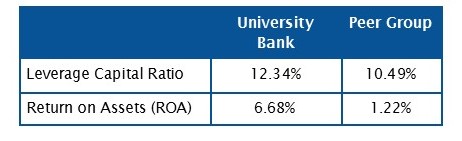

Now for a traditional community bank, 5-Star University Bank—Ann Arbor, MI. It is locally owned, locally managed and serves the local businesses and residents of Ann Arbor and Ypsilanti, Michigan. University Bank, originally chartered as Newberry State Bank in 1908, has several subsidiary companies that offer insurance and mortgage needs as well as faith based financing.

In comparison to its peers, University Bank soars in areas of capital and income:

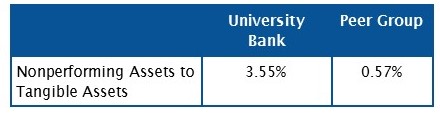

The same cannot be said for loan quality:

With robust capital, nonperforming assets don’t concern us. University Bank has a Bauer’s Adjusted Capital Ratio of 12.23% and a Texas Ratio of 1.33%.

These are three examples, but all 53 banks on page 7, whether via niche banking or good old-fashioned community banking, are finding ways to make money without overburdening their depositors. FSNB should take notes.