Commercial Real Estate (CRE) loans are comprised of multifamily (five or more) residential real estate, office buildings, shopping malls and most other structures that house businesses. Most of which have expanded along with the economy over the past several years. However, according to the 2019 FDIC Risk Review (released July 30, 2019), there is rising concern in some of these areas.

There is a surplus of both multi-family and industrial properties, but it pales in comparison to that of retail. As consumers have shifted toward online shopping and away from shopping malls, the smaller retail markets in the Southeast and Southwest, in particular, have proven particularly vulnerable.

To compensate, according to the report, FDIC-insured banks have shifted their lending toward existing properties and relying less on new construction than they had in the past. That may be, but we see more to it than that.

We are hearing banks talk about pulling back from CRE lending in their second quarterly earning calls. Will it be enough? To soon to tell.

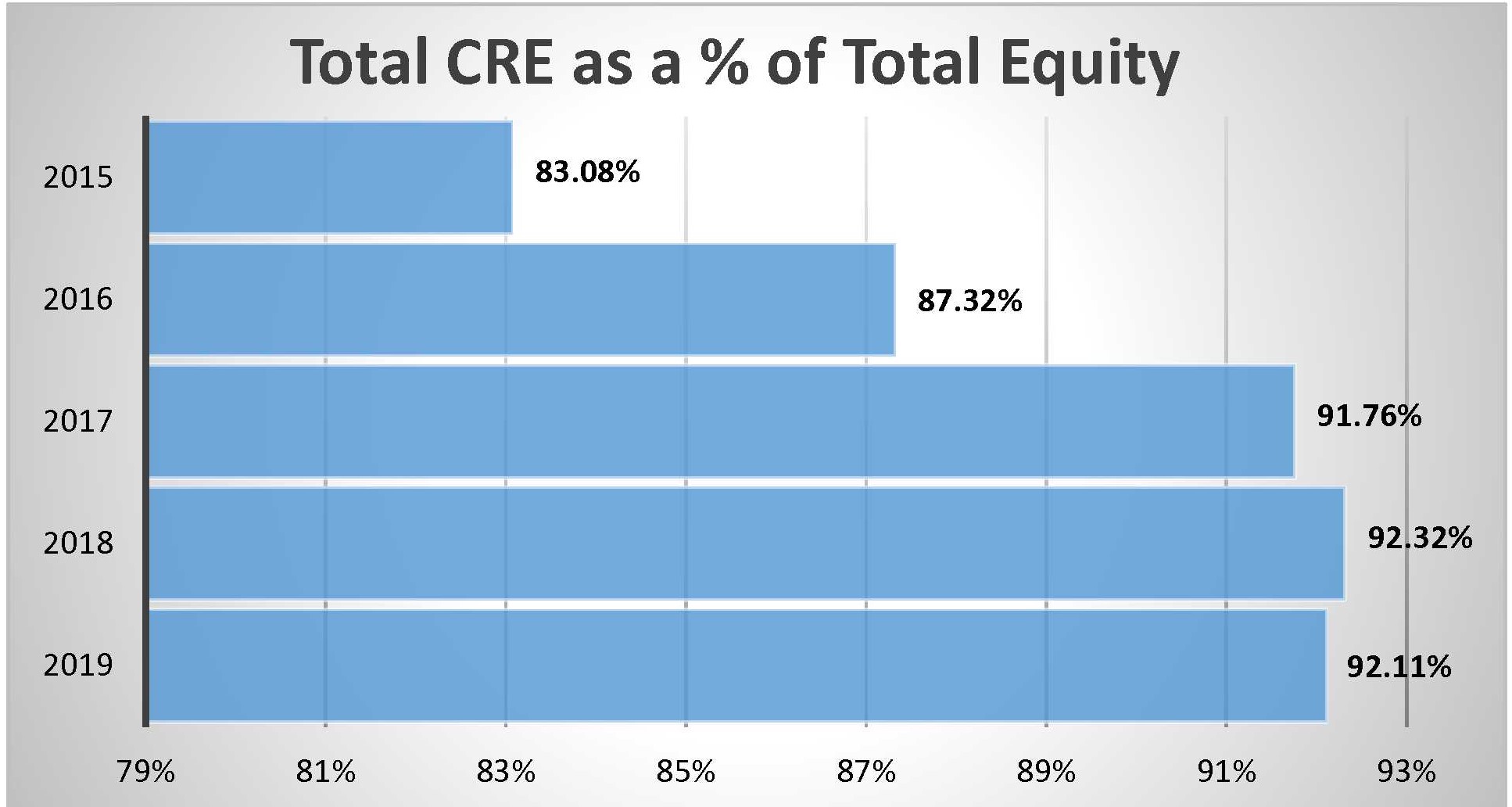

According to 1st quarter call report data, total CRE loans (including multi-family) as a percent of total equity dropped a mere 21 basis points between March 31, 2018 and March 31, 2019. While second quarter earnings calls suggest that pullback will increase, they have a long way to go (see graph).

Also released last month was The Beige Book (July 17th) adding some new and interesting developments to the picture. While the Summary would have you believe that the nation is enjoying a double dose of higher CRE prices and a greater number of CRE transactions, there are clearly concerns, including:

· Weakening macroeconomic outlook;

· High material and labor costs;

· Flooding in the Midwest and Texas;

· And a decreased appetite for new permits.

More important than the quantity of loans, is the quality of those loans. Proper underwriting is arguably the most important aspect of banking. A lot of banks lost sight of that before the last crisis and hundreds no longer exist as a result.

The banks listed on page 7 of this week’s Jumbo Rate News have three things in common. They each have:

- at least 25% of total loans in CRE;

- 10% or more growth in CRE loans during the 12 month period ended March 31, 2019; and

- at least 2.75% of the CRE loans are 90 days or more past due.

You may be wondering how so many of these banks can be rated 5-Stars. Of course each case is different, but lets take a look at 5-Star rated Muenster State Bank in Texas. It stands out since it is the only 5-Star bank on the list with a double digit delinquency ratio.

First of all, Muenster State Bank’s loan to deposit ratio is way below normal at just 33%. Plus, it has just over the 25% threshold we used for CRE for this list—25.1% to be exact. And although 12.3% of those CRE loans are 90 days or more past due, the other 74.9% of its loans are stellar. Its overall delinquency to asset ratio is 0.86%. All of its capital ratios are impressive as well:

Leverage CR: 14.91%

Total Risk-Based CR: 37.13%

Tier2 Risk-Based CR: 38.10%

Bauer’s Adjusted CR: 14.17%

and Texas Ratio: 5.62%

Muenster State Bank serves North Texas through a headquarter office in Muenster as well as a full-service branch in Gainesville. Since 1923, it has provided the agricultural and land development assistance the community has needed, as well as provided financing for oil and gas that was discovered in the area in the 1920s.