Commercial Real Estate (CRE) loans are comprised of multifamily (five or more) residential real estate, office buildings, shopping malls and most other structures that house businesses. All of which expanded along with the economy over the past several years. And all are suffering now along with the rest of the economy.

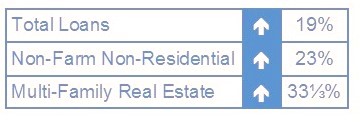

The largest subcategory of CRE, non-farm, non-residential real estate, was up 4.8% at the nation’s banks during calendar 2019 and now exceeds $1.5 trillion. Multi-Family housing was up even more (6.6%) during 2019, but look at the increases over the last 5 years:

Even before we were mandated to shelter at home, and even in the midst of a historic economic expansion, concern was already beginning to build. Last summer we first reported on the new “Ghost Mall” phenomena (JRN 36:30) as U.S. consumers were becoming increasingly accustomed to the conveniences of online shopping.

In the past month or so, that convenience has turned into necessity and even obsession for many of us.

Some businesses will come through this pandemic unscathed. Some (i.e. Amazon) will even thrive. Unfortunately, many will struggle to keep their doors open—or reopen them, as the case may be.

This is precisely why the adage says, “Don’t put all your eggs in one basket”. If something happens to that basket, you’ll be left with nothing. Most banks hold some CRE loans, which is good. But, too much CRE concentration (or of any concentration) could put a bank at risk in a market downturn, like now.

As the nation’s bank rating firm, it’s Bauer’s job to stay on top of these things (high concentrations, rapid growth, bad loans, etc.). While they do not automatically translate to impending problems, they must be monitored carefully.

Due to the growing surplus in industrial properties and increasing possibilities of non-paying renters, CRE loans will be among the first to be hit by COVID-19.

Given that, we have 52 banks listed on page 7 that have three things in common:

- Non-farm, non-residential (NFNR) Commercial Real Estate loans represent at least 25% of total loans;

- These loans increased by a minimum of 10% during the 12 months ending December 31, 2019; and

- At least 2.25% of those loans are 90 days or more past due.

This DOES NOT mean the banks are in trouble. In fact, as you can see many are rated 5-Stars or 4-Stars by Bauer, which examines the complete financial picture, history and business model of the institution.

For example, 5-Star T Bank, N.A. in Dallas is number four on the list because over 50% of its loans are in NFNR, but that is the business model of this particular bank. Its purpose is to help local business grow and thrive. In fact, another 43% of its loans are dedicated to commercial and industrial loans and another 4% to construction and land development. That doesn’t leave much for anything else.

And, as long as it adheres to proper underwriting, that’s okay. Based on year-end financial data, T Bank has total assets of just under $360 million. About $300 million of those assets are loans and about half of those are non-farm, non-residential loans.

But there is a lot you don’t see on page 7. For example, its assets and equity both grew at a good clip last year (not just loans). Assets grew 17% and equity 29%.

In addition, T Bank has a leverage capital ratio exceeding 11% and CET1 and risk-based capital ratios all exceeding 15%. All are well above regulatory requirements.

Its past due loans and nonaccrual loans are a bit high, which bears watching. However, its Texas Ratio of 2.8% is well below other banks of its size, which average about 5.3%. Remember, the ideal Texas Ratio should be as close to zero as possible. The higher it gets, and the closer it gets to 100, the more likely it is that the bank will get in trouble due to bad loans. All this to say, trust the star-ratings. We’ll do the hard part.